In the retail realm, it’s a clash of the titans: Walmart, the world’s largest retailer, versus Amazon, the online giant that aspires to be “the everything store.” Both are slashing prices and increasing free, same-day and other enticing delivery-and-return services in pursuit of market domination. Amazon’s online savvy and forbearance of profit-taking are well known. Walmart, with its vast bricks-and-mortar network, is finally getting serious about e-commerce.

But with two, not just one, behemoths now cutting into profit margins in a race for market share, what are the consequences for the rest of retail? “If those two keep getting better, it’s going to be rough news for other people,” says Wharton marketing professor Stephen J. Hoch.

Retail futurist Doug Stephens also sees “huge” potential for collateral damage to other retailers. “I think we are already seeing it,” he notes. “Target issued a letter, though it was more of a directive, to its vendors a year and a half ago that said if you sell us anything we later find on Amazon, you run the risk of being delisted as a vendor. This is very serious for every retailer — be careful of the shrapnel flying around as Amazon expands into other categories.”

According to Wharton emeritus marketing professor Leonard Lodish, “Amazon and Walmart are going to take over the market for people who want stuff cheap and fast. Who will win is up for grabs.”

And what Walmart and Amazon do has a way of trickling down: “There is definitely pressure on all retailers to increase speed and lower the cost,” notes Matthew Nemer, a managing director at Wells Fargo Securities covering the retail and e-commerce sectors.

The race to provide instant gratification has intensified in recent weeks, with eBay’s acquisition of Shutl, a same-day — and same-hour — delivery service based in the U.K. with service in New York, San Francisco and Chicago. The purchase will help eBay expand the service into 25 markets by the end of 2014. Last year, Google bought BufferBox, a shipping kiosk service that places boxes inside of stores like 7-Eleven to accept delivery of merchandise, enabling customers to pick them up at their convenience.

“Amazon and Walmart are going to take over the market for people who want stuff cheap and fast. Who will win is up for grabs.” –Leonard Lodish

Amazon, which has a similar pick-up service called Locker, is operated from Procter & Gamble warehouses in an effort to cut delivery times for household goods, The Wall Street Journal reported recently. Even the venerable U.S. Postal Service is getting in on the e-action, having just signed a deal to deliver Amazon’s packages on Sundays in some cities. The post office says it expects to make similar deals with other retailers.

Amazon’s business practices have produced a spark of protectionism in France, where, in a regulatory fit of pique, the Assemblée nationale approved a law aimed at defending independent bookshops. If passed by the senate, the law would prohibit retailers from offering free delivery on discounted books.

New Bricks and Mortar — for E-commerce

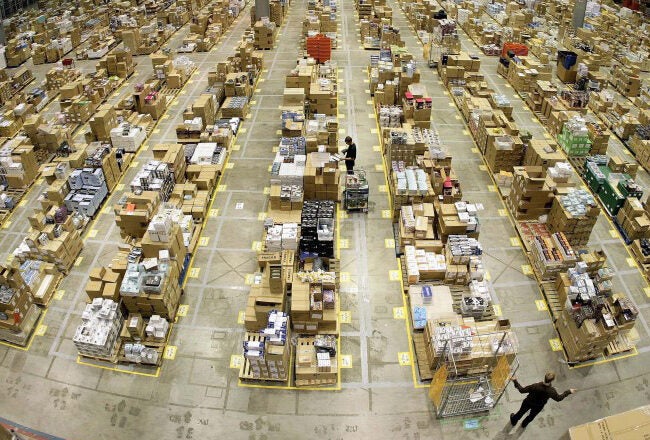

The Walmart-Amazon clash, many observers say, is part of a much larger battle compelling retailers to spend billions of dollars in new warehouses to facilitate quick delivery as the shift toward online shopping accelerates. Rather than luring the customer to the merchandise, the merchandise is going to the customer, and the industry is transforming itself. Amazon has funneled $13.9 billion into warehouses since 2010. Soon it will have nearly 100 warehouses to support what the company aims to make the new norm: orders shipped the same day the purchase is made.

Many of the warehouses being built by retailers are located close to urban centers — especially to the East Coast, where they will be within a few hours drive to as much as 40% of the U.S. population. Urban Outfitters is building a $110 million fulfillment center in Gap, Pa., the Philadelphia Inquirer reported recently. Macy’s, Nordstrom, Kohl’s, Bed Bath & Beyond and others have built, or are planning to build, similarly sized facilities.

“There’s a massive ecosystem being built around online sales — shipping, payments, mobile applications, electronic notebooks for store employees, lockers. I get an email every day highlighting all the venture capital investments going after some part of it,” says Nemer, adding that all of these developments point to a quickly evolving consumer mindset that expects same- or next-day delivery every time.

Yes and no, notes Lodish, who is also the leader and co-founder of the Wharton Global Consulting Practicum: “For a lot of products, people need it fast, like diapers and pharmaceutical products. For other products, I am not sure it’s that critical.”

Growth opportunities beckon to both Amazon and Walmart despite their dominance. Amazon is expected in 2013 to bring in $74.4 billion in revenue — all online. Walmart, with about $500 billion in revenue, is just skimming the surface of its online potential, with about $10 billion of that coming from e-commerce. Both have their eyes on forecasts calling for online to take an ever-increasing share of total retail sales. Online retail in the U.S. is expected to grow at a compound annual growth rate of 9% through 2017, according to Forrester Research. Some believe a third of sales will be conducted online by 2022.

“What is advertising, what is distribution, what is online, what is shopping? These words are passé. It’s terribly exciting.” –Barbara Kahn

But Barbara E. Kahn, director of Wharton’s Jay H. Baker Retailing Center, says that to focus on the Amazon-Walmart turf war is to miss what’s really going on now. “Think bigger — much bigger,” she notes, citing Google Shopping Express, a delivery program launched in limited markets in which the search engine partners with Target, Office Depot, Walgreens and other retailers to give member customers same-day delivery of orders. “Why is Google in this space when their revenue model is built on advertising? Why is their area now delivery?” Kahn asks. “Because Google makes its ad dollars through searches, and if you are shopping on Amazon and you are not searching for that item through Google, then Google is losing the search, and that is where the revenue is. These worlds are blurring.”

Websites like Net-A-Porter further exemplify the trend. In the online magazine styled with vaguely mimicked Vanity Fair graphics, consumers can currently read about how women’s fashion is borrowing aesthetic inspiration from men’s suits, or how much it costs to take a bespoke vacation in Istanbul (from £14,700 — US$23,380 — per person for three days). But readers can also buy what they see, simply by moving their cursors to the top tab.

“What is advertising, what is distribution, what is online, what is shopping? These words are passé,” says Kahn. “It’s terribly exciting.”

Smaller Retail and Evasive Action

According to observers, one vulnerable sector is museum shops and other retail outfits attached to cultural institutions, where books still account for 25% to 35% of sales. The best defense for them — and other small retailers in general — is to move further into merchandise that can’t be found elsewhere. “They have to become a lot more aggressive in terms of carrying things that Walmart and Amazon do not,” notes Joan Doyle, principal of doyle + associates, which works with specialty and cultural retail clients. “They have to become places of the unique and the unusual, and that has to be constant. When someone can’t comparison shop, then Amazon becomes a moot option.” Lodish agrees: “There is a whole slew of retailers who have differentiated products that aren’t even being touched,” in the inventory offered by the major players.

Another strategy for smaller retailers: If you can’t beat ’em, join ’em. EBay can supply the networks for businesses that can’t compete now, suggests Kahn. “If they can partner, then they can compete.”

‘Get Big Fast’

Those who do cross swords with Amazon and founder Jeff Bezos, though, do so at their own peril — including, perhaps, Walmart. “Walmart would be stupid to try to go head-to-head too much with Bezos,” states Hoch. The problem, he notes, is that Amazon is out to increase market share and willing to forego profits to accomplish that. When this might change and what the end game is are not clear, says Hoch, who adds: “They’ve been doing this forever. I met a strategy person there in 1998 and asked her, ‘What is the business plan?’ She said GBF — Get Big Fast. And they are still following that strategy. For a while there it looked like they were going to make a little bit of money. Then they decided not to. It’s kind of weird — Jeff Bezos can just decide whether or not to make money.”

“They have to become places of the unique and the unusual, and that has to be constant. When someone can’t comparison shop, then Amazon becomes a moot option.” –Joan Doyle

Both Amazon and Walmart are “willing to lose money in certain categories, and it’s got to be difficult for anyone in those categories,” says Wharton marketing professor David Bell, who points out that the two giants have been moving into the same space for some time — including one well-documented skirmish. In his book, The Everything Store: Jeff Bezos and the Age of Amazon, Brad Stone tells the story of how Amazon and Walmart both wooed Quidsi, the start-up behind Diapers.com. Amazon won, though not until Bezos engaged in some rather ruthless tactics. (The book, by the way, lists on Amazon.com for $17.47, a 38% discount off the publisher list price.)

But Nemer cautions against underestimating Walmart, which now has five million items for sale on its website (including Stone’s book on Bezos for $16.80, a 40% discount below cover price). “The competition between Amazon and Walmart is still not really appreciated by a lot of people,” he says. “Most folks think Amazon has a huge lead, and are not aware [that] Walmart plans to continue expanding in this area. If you ask most people how many employees Walmart has in online, they will say a number in the tens or maybe hundreds. It’s in the thousands. They are making great progress — they already have.”

To Nemer, the biggest thing that Walmart lacks is a loyalty program like Prime. “Amazon’s strength is Prime. It drives your frequency on Amazon. So the trick for Walmart is to do a loyalty program, and I think they are working on it. This is the one thing that could change the shape of the curve.”

For the entire sector, Stephens describes what is playing out now as nothing short of epochal. “We are coming off this 50- to 60-year period where if your business had a relatively good product and a decent location, good prices and not a bad marketing program, you could make money,” he notes. “You controlled the path of purchase, and the customer didn’t have an alternative. Clearly we are not in that world anymore. Customers have a wealth of options in their pocket. And I think we are going to continue to see fallout…. With every move of Walmart or Amazon going into a different category, you are going to continue to see damage.”