The following opinion piece was written by Wharton senior fellow and finance lecturer David Erickson. Erickson is also co-director of the Stevens Center for Innovation in Finance. Prior to teaching at Wharton, he worked on Wall Street for more than 25 years, helping private and public companies strategically raise equity.

While the public equity markets have had a difficult run since hitting their peak in late 2021, the private equity markets continued to “chug along” until mid-2022, when the U.S. Federal Reserve started its historic interest rate tightening. Unfortunately, with the IPO market freezing up and the M&A market slowing down considerably last year, the ability of private equity firms to monetize their existing holdings also slowed down considerably. For many funds, this has caused their returns to suffer. In private equity language, IRRs (Internal Rate of Return) are slipping because it is taking longer to monetize; and MOICs (Multiple of Invested Capital) are falling as their value “marks” are deteriorating with the public markets.

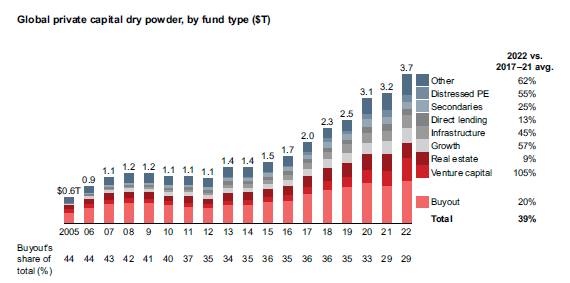

According to Bain & Company’s Global Private Equity Report 2023, at the end of 2022, there was a record amount of approximately $3.7 trillion of dry powder (private equity cash reserves) looking to be deployed globally. As can be seen in the below chart, this amount spans the breadth of the global private equity landscape from buyout to venture capital to infrastructure to real estate and distressed private equity:

So, what’s wrong with Private Equity? I would suggest there are three primary issues:

- FOMO (Fear Of Missing Out) Has Turned Into DWTCAFK (Don’t Want To Catch A Falling Knife)

- The Federal Funds Rate Changed the Math

- Large LPs (Limited Partners) Want More Involvement/Input

Let’s provide a little more context.

FOMO Has Turned into DWTCAFK

Since the collapse of FTX last fall, there has been lots of discussion about how many of the largest and most successful private equity firms were fooled into giving FTX money at increasingly higher valuations. Just over a year ago, FTX closed its last round of $400 million at a $32 billion equity valuation. This was up from the $25 billion valuation it had raised only six months earlier. After the FTX collapse, one of the most successful and largest venture capital firms, Sequoia Capital, was led to apologize to its investors about their FTX investment.

Fast forward to the last few weeks when Stripe, one of the most highly valued and successful “unicorns,” was reportedly raising approximately $4 billion at a $55 billion valuation — almost half the valuation the company had in 2021. Despite the fact that investors (including Sequoia) were lining up to give Stripe money at a $95 billion valuation two years ago, the current fundraise has struggled. The Information reported at the end of February that Stripe was dropping the valuation by another 10%. A high-profile example of FOMO turning to DWTCAFK — unfortunately, probably not the last.

The Federal Funds Rate Changed the Math

A year ago, the U.S. Federal Funds Rate stood at 25 basis points. As of this writing, the U.S. Federal Funds Rate stands at 4.75%, with the market currently expecting another 25 to 50 basis points later this month. Obviously, with this potential 500 basis point change in a year, the math to investing (and generating a significant return) in a company, especially one that is reliant on debt, has changed considerably for private equity firms. In addition, last week’s collapse of Silicon Valley Bank, a key player in the early stage/venture capital ecosystem, shows how risks continue to rise for venture capital firms and their portfolio companies. This comes at a time when the biggest percentage year-over-year increase in dry powder (as shown in the chart above) is in venture capital at 105%.

Large LPs Want More Involvement/Input

Some recent articles have referenced the “denominator” problem as a key factor impacting private equity fundraising. (The denominator problem is when private equity LPs have a specific percentage allocation to private equity that can be limited if another large allocation — e.g., public equity — significantly decreases in value.) While this is a factor, I believe a bigger reason is that with declining returns and the huge amount of dry powder available, many large LPs (who can make or break a fundraise) are increasingly expressing interest in taking a more active role in portfolio decision-making along with their financial commitment (and their considerable fees paid).

“Like in every industry, there are underperforming private equity firms that in a strong market survive; but in the current markets, they should probably get weeded out.”

What Will Fix Private Equity’s Problems?

Here are three places to start:

1. Go Back to the Basics

While not as headline-grabbing as investing in companies like Stripe or other high-profile unicorns, the more traditional deals that made private equity the most money consistently over the years included companies where PE firms invested; grew the business by improving operations and helping the company scale (including potentially assisting with acquisitions); and exited through a sale or an IPO/equity monetizations. Back in the early 2000s, when the IPO market started to re-emerge (after the Tech Bubble), it was largely driven by these private equity-backed companies across sectors that generated positive cash flow and operated in attractive end markets. Seeing similar companies come to market soon could have an improving effect now, too.

2. Give Back the Money

As companies stayed private longer and valuations went higher (i.e., Stripe), more and more private equity firms raised larger funds to continue to fund these larger rounds, especially in the late-stage growth equity market. Unfortunately, that market has changed dramatically and many of those opportunities have also changed (e.g., Stripe). As a result, if the market reward-risk dynamic has significantly changed, while nobody likes to give money back, doing so will probably build more trust with LPs over both the short and long term. This occurred after the Tech Bubble burst back after 2000 with firms including leading firms such as Mohr Davidow, Kleiner Perkins, CRV, and Redpoint Ventures cutting the size of their funds. According to Axios, Founders Fund recently announced that they were cutting their eighth fund in half, to $900 million. With approximately $3.7 trillion of dry powder and the current reward-risk profile in some areas having changed dramatically, like we saw 20 years ago, many more firms should probably give back the money (or at least “right size” their fund).

3. Weed Out Underperforming Private Equity Firms

Like in every industry, there are underperforming private equity firms that in a strong market survive; but in the current markets, they should probably get weeded out. The large LPs should ensure they also do their due diligence (much as they chided FTX investors in the wake of its collapse). If a private equity firm whose recent funds have severely underperformed (i.e., their most recent funds are consistently in the 3rd and 4th quartile) comes calling for their newest fund, maybe the answer should be no.