“A decentralized approach towards global agriculture may ensure that supply meets growing demand requirements, while also encouraging equitable participation regardless of geography,” write the authors of this opinion piece. They are Michael Ferrari, managing partner of Atlas Research Innovations , who is also on the faculty advisory committee for the Wharton Initiative for Global Environmental Leadership. His work focuses on the technology-environment-infrastructure nexus, emphasizing global commodity strategy, and data science and analytics. Parag Khanna is managing partner of FutureMap. He is the author of the new book The Future is Asian. Part 1 of this two-part series looked at how the Belt and Road Initiative (BRI) portends significant shifts in the dynamics of the global agricultural trade.

Here in Part 2 they examine some of the physical risks that will accompany BRI expansion, and offer thoughts on the future agricultural supply chain.

The expanding agricultural commodity complex promises to include more buyers and sellers and with new trade routes re-opened that have long been dormant. While this is fertile ground for emerging market opportunities, there are also risks — both acute and subtle — to this expanding agriculture trade. Here we examine some of those risks in greater detail.

Consumption Risk

The first supply side risk is largely behavioral and in turn magnifies other risks. Overconsumption, and the resultant byproduct food waste, is perhaps the most important risk as it is predicated upon choice. Having a seemingly infinite selection of choices, year-round, seems like a positive byproduct associated with financial security. But being able to purchase pineapples in New York in February carries a cost: A large number of resources, chief among them water and fossil fuels, are utilized to attain a food-on-demand world. Further, this conveyor belt of continuous supply depletes soil, water, and biological resources at an unsustainable pace. Efficiency gains resulting from growing technologies and infrastructure expansion and improvements will help, but they may actually exacerbate the problem when the consumer demands continue unabated.

This also does not even begin to address the important but oft-overlooked distinction between food security and nutrition security. Today, we may have the technology network in place so that we are able to feed the population (some argue that hunger is more of an access issue than a production one), but for much of the world the calories consumed are empty. In other words, access to cheap mass-produced food with refined grains as the staple ingredient is not providing the adequate nutritional benefit commensurate with daily calorie consumption. If we are to look at food sustainability seriously, as population centers in the east are growing at a faster rate than their western counterparts, the provider community should be looking to develop affordable food products that carry and retain the nutrition present when the crops were harvested.

Physical-Climate Risks

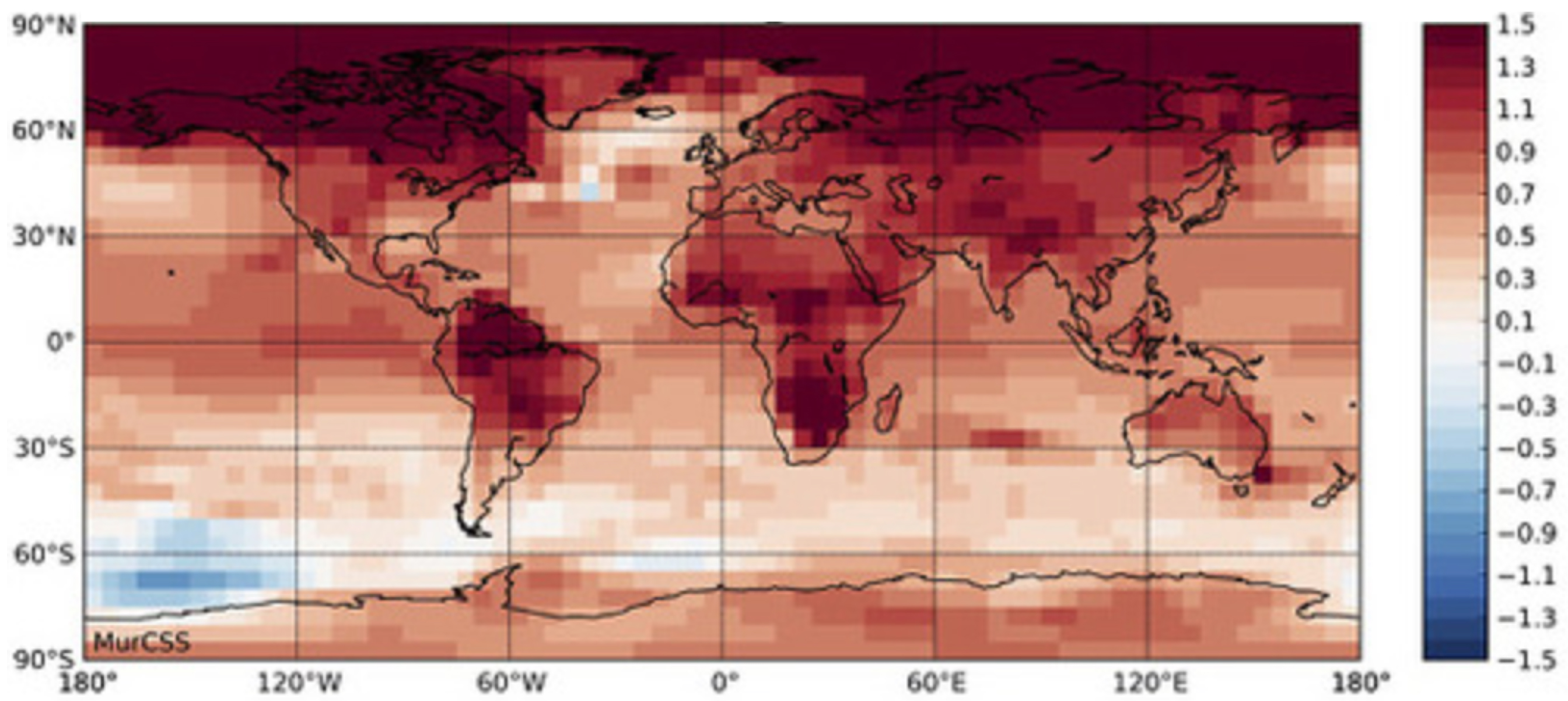

Weather-crop disruption is the first climate related consequence. Extreme and acute examples come to mind first: widespread drought decimating the Brazil coffee crop in 2016, U.S. corn in 2011 (see price chart below), and Australian wheat in 2016. Excess precipitation can be equally devastating as the global grains complex is currently coping with the effects of flooding in the U.S. Midwest, Brazil, Central Europe and several former Soviet republics. Less publicized but equally damaging can be the slower insidious risks that develop over decades, including a lowering of the water table, the trend of increasing evening temperatures, and multiple consecutive days of triple digit temperatures.

All of these culminate in reduced supply and lower yields. Regardless of the causes, climate change and variability will alter the way commodity products are grown, how they are distributed, and even consumed against the backdrop of a growing and more affluent global population. With changes in climate, there will be winners and losers with respect to growing origins. While we can use long range models as a guide, many of the significant changes important to agriculture are expected to continue to occur between latitudes of 30 degrees north and 30 degrees south, as noted on the map above depicting projected global mean temperature anomalies changes for 2015 to 2022 versus the 1971-2000 reference period. New varieties and new origins will likely need to be developed or converted for production, and much of this potential expansion in farmable land will benefit producers operating along the transect of Belt and Road Initiative (BRI) participating countries in the East where projected temperature rises may not be as extreme.

Water and Climate Risks

Perhaps more important than changes in temperature will be how temperature shifts manifest the movement, availability and distribution of fresh water across the continents. Decadal climate models project a continuation of ongoing trends: Typically wet areas will get wetter, and moisture-deficient areas will get progressively drier. Water, and more appropriately the lack of water, is a tricky problem to anticipate. Unlike other environmental resource issues where there is often times an acute trigger before a collapse, water deficiencies can have multiple competing factors, and the onset of a problem is somewhat masked; that is until it becomes an ‘event’ and there are no viable supply alternatives.

Changing water dynamics will alter not only the varieties of annual crops that can be supported in certain geographic regions, but will also impact the investment cycles around longer maturing assets such as tree crops. These perennial biological assets, once planted, are expected to produce commercially viable yield quantities for decades. Beverage plants are another example of physical assets with a longer time horizon underlying ROI. A change in water availability one or two decades after a capital expenditure in these industries complicates the calculus of risk and return.

The water dynamic needs to consider not only the food production component, but also what happens when a ‘commons’ resource is depleted and the surrounding population suffers the effects. This issue was highlighted most dramatically in recent years when bottling plants affiliated with The Coca-Cola Company (Coke) were held largely responsible for a reduction in freshwater supplies across India and Latin America. Since then, Coke has taken ownership of this issue and started to implement a series of precautionary measures to ensure that this situation is not repeated. Further, they have pledged to ensure that communities in regions where they operate are provided with a more favorable water balance situation than they had prior to their arrival. How this unfolds in the decades to come in the face of accelerated climate change, however, remains to be seen.

Financial Climate Risks

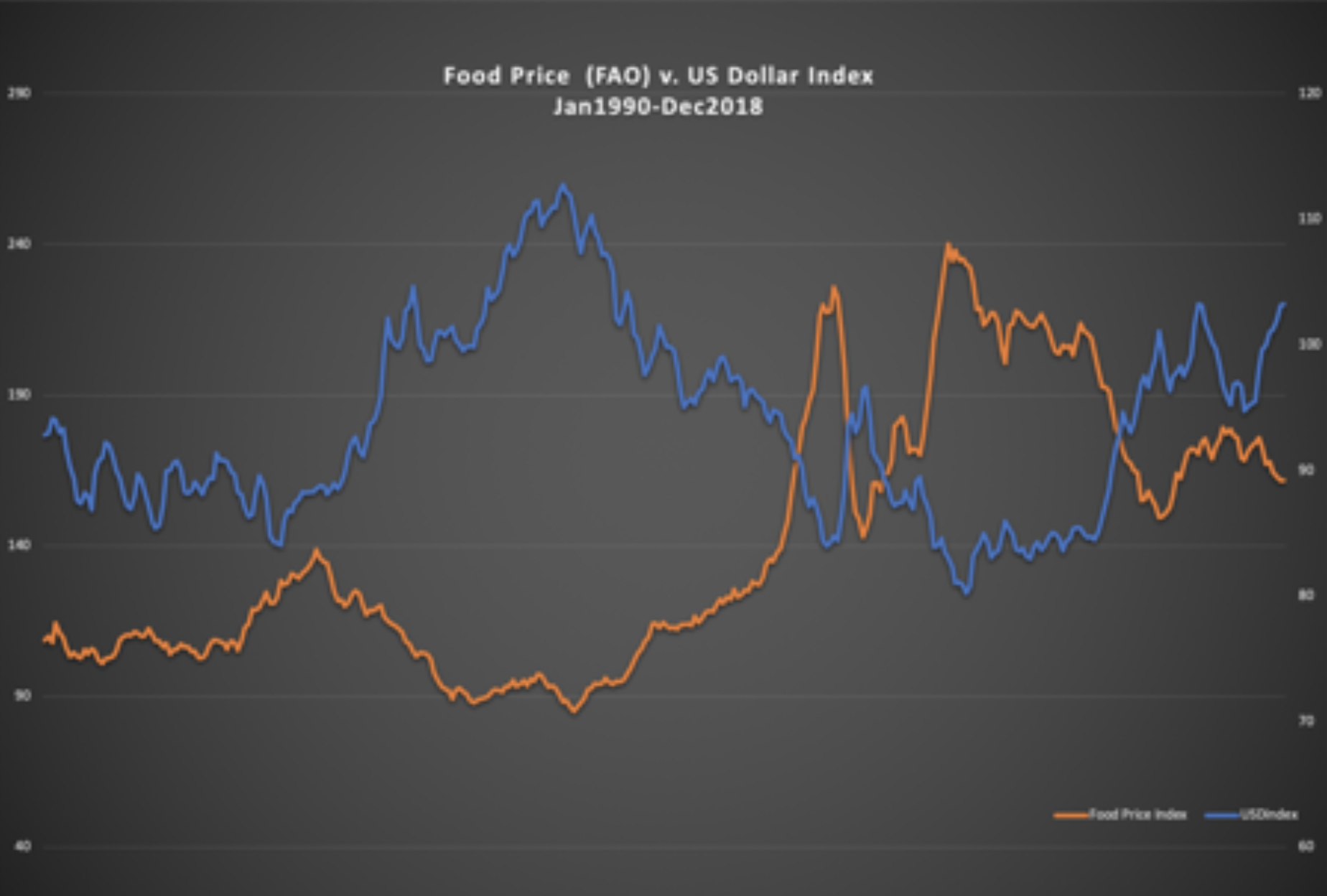

Accompanying climate driven changes in the supply side will be another big risk in the liquidity of commodities: Foreign exchange. Using the U.S. dollar as the global commodity benchmark, the ‘typical’ relationship between currency and commodities has been inverse: A stronger dollar tends to correlate with a suppression of food prices. The chart above shows a high level relationship between U.S. dollar and the global Food Price Index as determined by the United Nations Food and Agriculture Organization (FAO). Analysts typically look for this foreign exchange relationship to signal price reversals. While this is a generalized rule, it does not always hold true, and it is likely to erode further as Asian nations become more important players on the global agriculture stage. A growing number of regional exchanges around the world have started to offer liquid futures and options contracts for commodities, decentralizing the risk and in the process reducing the importance of contracts which originate in New York, Chicago or London.

Accompanying climate driven changes in the supply side will be another big risk in the liquidity of commodities: Foreign exchange. Using the U.S. dollar as the global commodity benchmark, the ‘typical’ relationship between currency and commodities has been inverse: A stronger dollar tends to correlate with a suppression of food prices. The chart above shows a high level relationship between U.S. dollar and the global Food Price Index as determined by the United Nations Food and Agriculture Organization (FAO). Analysts typically look for this foreign exchange relationship to signal price reversals. While this is a generalized rule, it does not always hold true, and it is likely to erode further as Asian nations become more important players on the global agriculture stage. A growing number of regional exchanges around the world have started to offer liquid futures and options contracts for commodities, decentralizing the risk and in the process reducing the importance of contracts which originate in New York, Chicago or London.

As more regional exchanges appear, two things follow. First there is the availability of a decentralized liquid market, which is the necessary fuel for price discovery. Many market transactions work on paper, then fall apart when faced with real world risk. As markets need buyers and sellers, liquidity brings more participants to the table and lowers the barrier to entry for new-origin participants. Second, once liquidity reaches a critical mass, well-functioning markets offer financial instruments such as futures and options, which in turn attracts additional capital liquidity and more market entrants. As price transparency starts to emerge, a more equitable platform for buyers and sellers results. As more BRI participant companies grow to become major commercial supply-side players, we should expect to see the U.S. dollar relationship as the global benchmark diminish in prominence as new commodity-currency relationships emerge.

Disease Climate Risks

Changing climate patterns may also enable or suppress the conditions that lead directly to plant or cultivar disease. Moreover, these mechanisms indirectly alter the biomes that disease transmitting vectors call home. Both scenarios can lead to an increase in risk to the food system. There is already evidence over the last few decades documenting the expansion or migration of biogeographical parameters related to certain species’ survivability ranges. As temperature shifts, this can lead to the forced migration into/out of traditional biogeographic delineations. As non-endemic species travel into new ecosystems, existing flora and fauna comprised of plants, pollinators and parasites, all are subject to new evolutionary pressures they are not equipped to handle.

Evolutionary ‘fitness’ is tested within one or two generations. Technology can help to protect against some of the stresses, but in the biological arms race, traditional monoculture, the de facto method for most commercial agriculture, is increasingly at risk of collapse. Monoculture cropping is efficient at producing large quantities of food and fiber, with limited diversity, at scale, and this seems to make good sense. Biology tells us otherwise. Limiting genetic diversity on the supply side leads to susceptibility to disease – particularly those diseases whose vectors have roots in rapidly changing environmental conditions. Biomes in tropical regions where expanding temperature habitability ranges are attractive to microbial invaders immediately come to mind.

Further, climate change will only exacerbate this potential problem on a global scale.

Contagion Climate Risks

This cursory overview of the risks described above should highlight the precarious nature of the global food supply network. However, while each of these individual risks carries significance, when one or more of these factors occur in a short duration, we potentially move into threat-multiplier territory. The cascading effects from supply disruption in one market can easily spill over into several other markets, and this in turn reintroduces additional pressure on underlying foreign exchange risk.

When supply origins are in an unfavorable currency position, and physical material and product decisions for delivery several months forward are shifting in near-real time, the fallout can be severe. Again, low-margin producers get squeezed and bear the brunt of the losses. We have seen this play out numerous times on a smaller scale with Latin American and East African origins, and with BRI opening up avenues for new trade partners, the likelihood of increased risk, and the subsequent effects of contagion will surely heighten.

For a reminder of potential contagion risk, recall the Arab Spring protests from 2011. While this was undoubtedly the consequence of myriad contributing factors, one of the key catalysts for this event was tied to the ability of citizens to access ingredients to make or purchase bread, namely milled wheat. By 2010, numerous Arab countries had Russia as their largest wheat supplier, but Russia’s heat wave and drought that summer forced Moscow to ban wheat exports, leading to a significant spike in prices for which Arab governments were unprepared to respond. We of course cannot say for sure that having access to additional supply markets would have prevented the Arab Spring. Again, if we apply a blend of the precautionary principle with basic functioning of biological systems via evolutionary fitness, we could argue that redundancy (expanded supply) favors the prepared when faced with stress, and monoculture (limited supply or resources) is the precursor to bottlenecks, adaptations and collapse.

The (Belt and) Road Ahead

It is no secret that traditional agricultural commodity traders have experienced a difficult time maintaining an edge in the hyper-competitive market space in recent years. The BRI will change that. As more data has become available to an ever -increasing number of market participants, longstanding commodity corporations that once dictated physical and financial stocks and flows no longer have eminent domain with respect to market-moving information.

As a result, funds have closed, banks have sold off entire commodity units, asset managers have literally become a commodity themselves, and high frequency traders are picking up the financial crumbs. But this in no way supports the notion that the commodity complex does not have massive opportunity, particularly with more decentralized and inclusive global trade.

With BRI and other evolving network partners operating with one another, countries that had no previous relationships can become trading partners within months. Further, many models that were built and quantified on historical trade partnerships no longer have merit. As an increasing number of supply-side entrants will now be contributing physical agricultural supply to a world market which demands more products with greater diversity, suddenly any given country’s currency is now exposed to that of every other country in the world. It is not just the strength of the dollar versus the real/renminbi/rupee, but rather the dollar versus any country of choice.

Being able to navigate through this new interconnected world where borders are less important than regions is where the smart money should be placed. The BRI, and other forthcoming initiatives that might choose to replicate this example, may hold the potential to serve as the only viable means to sustainably feed the world. We maintain that the expansion or the diversity with respect to supply-side sources in commodity networks coupled with lower-cost and low latency technological solutions, can dissolve barriers to entry for emerging market participants, while at the same time providing opportunity and hedging risk.

Global infrastructure connectivity and integrated markets further propel us towards a supply-demand world of more decentralized service providers and equal access to resources, essential conditions for our collective survival and stability in an unpredictable world. A decentralized approach towards global agriculture may ensure that global supply meets growing demand requirements, while also encouraging equitable participation regardless of geography. Bringing food and fiber to the world while minimizing origin control by a few large players may be the only way that these challenges can be met.

Michael Ferrari is the managing partner of Atlas Research Innovations, and is on the faculty advisory committee at the Wharton Initiative for Global Environmental Leadership. His work focuses on the technology-environment-infrastructure nexus emphasizing global commodity strategy and data science & analytics.

Parag Khanna is the managing partner of FutureMap. He is the author of the new book The Future is Asian.