Is the U.S. headed for a recession? Opinion is divided on that question, with many economists warning of a recession and Wall Street bulls saying those fears are overblown. The familiar precursors of a recession have arrived: an inverted yield curve and rising interest rates on the back of high inflation (8.5% in March), with COVID uncertainty and disruptions caused by Russia’s invasion of Ukraine thrown in.

The yield curve inverted on March 29 for the first time since 2019. That happens when short-term treasury bills attract higher interest rates than longer-term treasuries — a sign that investors are losing confidence in the economy. Meanwhile, Federal Reserve chairman Jerome Powell brought down the other shoe on speculation of higher doses of rate increases when he signaled a 50-point increase in May (earlier increases have typically been in 25-point bursts). He also wanted to move “a little more quickly” with shrinking the Fed’s asset portfolio in an effort to tame inflation.

The most widely accepted definition of a recession is two consecutive quarters of declining GDP. According to a forecast by The Conference Board, U.S. real GDP growth will slow to 1.5% in the first quarter of 2022, down sharply from 6.9% growth in the last quarter of 2021. The White House is confident of strong GDP growth in 2022 despite inflation risks, and the International Monetary Fund shares that optimism with an estimate of 3.7% GDP growth this year for the U.S.

All Eyes on the Fed

The Fed has the wherewithal to stave off a recession, according to Wharton’s Susan Wachter, professor of real estate and finance, and Nikolai Roussanov, finance professor. “The main cause that would trigger a recession now is a spike in interest rates,” Wachter said. “The Fed’s actions so far and expected over through the end of the year will not in themselves trigger a recession.”

“If prices do not decelerate, as anticipated, the Fed faces a difficult path to a soft landing, which does not destabilize the economy.” –Susan Wachter

But the big question, according to Wachter, is what it would take for the Fed to slow the economy. “If war and pandemic shortages resolve, as the Fed expects, we can avoid an induced recession,” she said. “If not, the longer inflation persists the more likely we are to enter into a wage price spiral requiring the Fed to hit the brakes hard.”

“The U.S. economy is quite strong at the moment, but there is indeed some risk of slipping into a recession,” said Roussanov. “Its length and severity would depend in large part on the Fed’s response, and I expect it to do all it can to minimize the damage.”

Wharton finance professor Itay Goldstein is less optimistic. He noted that the onset of the pandemic in March 2020 is an important part of the background for the current debate. “The general expectation was for a longer and deeper recession, but when the data was analyzed in 2021, the conclusion was that the Covid recession was very short,” he said. “To a large extent, this was because of the fiscal and monetary intervention by the government and the Fed.”

Goldstein noted that those interventions contributed to the current inflationary spike, which warrants monetary tightening (with higher interest rates and a smaller Fed asset portfolio). “This has the potential to cause recession, which becomes more and more likely, as we see that the inflation problem is more severe than initially anticipated,” he said. “The geopolitical situation also contributes to these developments, making inflation worse.”

Inflation and Interest Rates

Powell had earlier last year described the Covid-induced inflationary pressures as “transitory” but later said they appear more powerful and persistent than expected.

“The main cause that would trigger a recession now is a spike in interest rates.” –Nikolai Roussanov

High inflation is likely to be a continuing phenomenon in the foreseeable future, Wharton finance professor Jeremy Siegel said recently on CNBC. “[The latest inflation rate of] 8.5% might be the peak, but [it will be] at 6% to 7% year-over-year for a long time. There are a lot of very negative forces in terms of making inflation worse.” For instance, oil prices have again crossed $100 a barrel, he pointed out. He added that he is “particularly worried about natural gas,” prices of which have almost doubled since the beginning of this year.

“Will we see something higher than 8.5% year over year?” Siegel wondered. “Maybe not, but is it going to be that good if it stays at 6.5% to 7%?” He noted the latest increase in core inflation (headline inflation minus food and energy) was lower than expected. “[Core inflation] is what the Fed looks at,” he added.

“The Fed would have to continue with at least 50-basis-point hikes for a number of meetings,” Siegel said. “The Fed really has to get [interest rates] above 3% to 3.5% if it wants to slow inflation, which I still think is OK.”

“While core inflation may have peaked, the Fed is under significant pressure to raise rates and unwind its balance sheet accumulated during the COVID period’s quantitative easing policy,” said Roussanov. “This pressure has already reverberated through the financial markets and is beginning to impact the housing market as well. The impending cooling of the latter, in particular, could have a negative effect on both consumer demand and some of the real activity (e.g. in the construction sector) that resembles the early stages of the subprime crisis [of 2007–2008]. It might be less damaging this time around though given the extremely tight labor markets, and could in fact help take the edge off the inflation spike.”

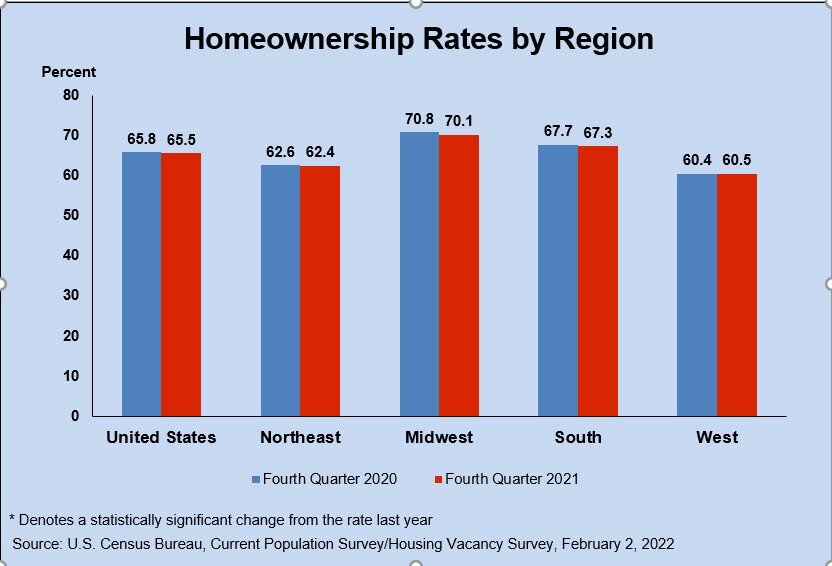

Home prices have soared to record levels, while home sales have fallen with rising mortgage rates, but there may still be room for optimism. “Mortgage rates at 5.25% already incorporate the Fed’s anticipated tightening,” said Wachter. “This is a significant and rapid increase in mortgage rates, but in itself, this will not reverse the supply/demand imbalance that is driving up house prices. With inflation at 8.5% as measured by the CPI (Consumer Price Index), borrowers are still motivated to buy. If inflation and mortgage rates fall, borrowers can refinance, as many have. Cash buyers are of course exempt from the mortgage rate spike.” Indeed, Wharton real estate professor Benjamin Keys recently said on Wharton Business Radio that he expected the dip in homebuying to be temporary.

“Will we see [inflation] higher than 8.5% year over year? Maybe not, but is it going to be that good if it stays at 6.5% to 7%?” –Jeremy Siegel

A sharp rise in interest rates and sharp decline in employment could, however, “bring turmoil to housing markets,” Wachter said. “Monetary tightening will work through mortgage markets. A soft landing is still the most likely outcome as the most recent CPI report shows that core inflation is coming under control. However, if prices do not decelerate, as anticipated, the Fed faces a difficult path to a soft landing, which does not destabilize the economy.”

Siegel noted the recent slowing in the rental and home ownership indexes, while home prices are up 15% to 20%. “[All that will] get into that [inflation] index,” he said.

Outlook for Capital Markets

Businesses may be able to weather the immediate impact of higher interest rates, especially those that in the past two years or so made good use of near-zero rates and bullish stock markets. “The impact [of costlier financing] on the financial side is tougher to gauge, although having had easy access to financing over the last couple of years most firms should have sufficient funds to maintain a healthy pace of investment,” said Roussanov. He noted that the 2007–2009 Great Recession was well underway when Lehman Brothers failed, “so it did not cause it per se, although the ensuing financial crisis surely helped deepen it.”

After last year’s bull run, the stock markets have turned volatile and the outlook is mixed.

Siegel agreed with other experts that corporate earnings growth, in general, would be strong. “That numerator is going to be great, but the denominator keeps on getting revved up,” he said, referring to the discount factor on earnings. “We have seen a very choppy market and a rotation, which will continue towards those stocks that have more near-term cash flows.”

“The stock market is in a fragile state, given that asset prices have been rising for a while, not always justified by fundamentals.” –Itay Goldstein

Siegel expected some moderation in technology stocks, which have seen much volatility so far this year after a strong run last year. “I’m not ready to say that technology [stocks are] off to the races, although there are a lot of tech stocks that are selling for fairly reasonable earnings [multiples] of 19–20 times. Anything more than that will be disadvantaged in this market.”

The stock markets show both early warning signals and the impact of economic downturns. “We already see wobbles in the stock market, and a further decline would be a good signal of an impending slowdown, which would then show up in GDP growth,” said Roussanov, who saw a mixed outlook for employment trends. Added Goldstein: “The stock market is in a fragile state, given that asset prices have been rising for a while, not always justified by fundamentals.”

How long would a recession last? Goldstein said the outlook is unclear on that question, “but given the expected actions from the government and the Fed, it might not be short.” He noted that the emerging economic scenario “is very different from recent episodes when the government and the Fed could more easily take steps to shorten the recession.” He did see a bright side, though, in the “strong labor market.” Roussanov added: “The job market is extremely strong right now with labor shortages everywhere, but we might see it cool off if there is indeed a significant contraction.”

{kind=link}