Uber stumbled out of the gate on its first day of trading as a public company last week to close below its initial public offering price, a rather awkward and inauspicious start to one of the most highly anticipated tech IPOs in recent memory. It didn’t help that shares of the ride-hailing giant debuted amid a volatile market roiled by the U.S.-China trade war, and got walloped as well on its second trading day following an equities rout. The stock remains under pressure, hovering well below its $45 IPO price.

But the bigger question is not the initial performance of Uber’s shares but whether the company will fare well in the long run — and prove itself to longer-term investors. “I’m not too worried” about Uber’s IPO performance, said Gad Allon, Wharton professor of operations, information and decisions, and director of the Jerome Fisher Program in Management and Technology. Other tech giants have overcome Wall Street’s initial jitters. “Facebook didn’t do well in the first few weeks, and it’s doing quite well now,” he said. “I’m worried because of other reasons.”

Allon said Uber was able to grow to its current size over the last few years in no small part by offering incentives, freebies and other promotions. “They have to subsidize drivers. They have to subsidize passengers to drive passenger growth … with the idea that ultimately there will be a winner takes all,” he said. “But one thing we know about this market is there’s really no winner takes all. It’s not even winner takes most.” And Uber’s mentality of “acquiring customers at any cost might result in a very strong valuation now” due to fast growth, he said, but the tricky part is to be profitable. “That might not be all that easy.”

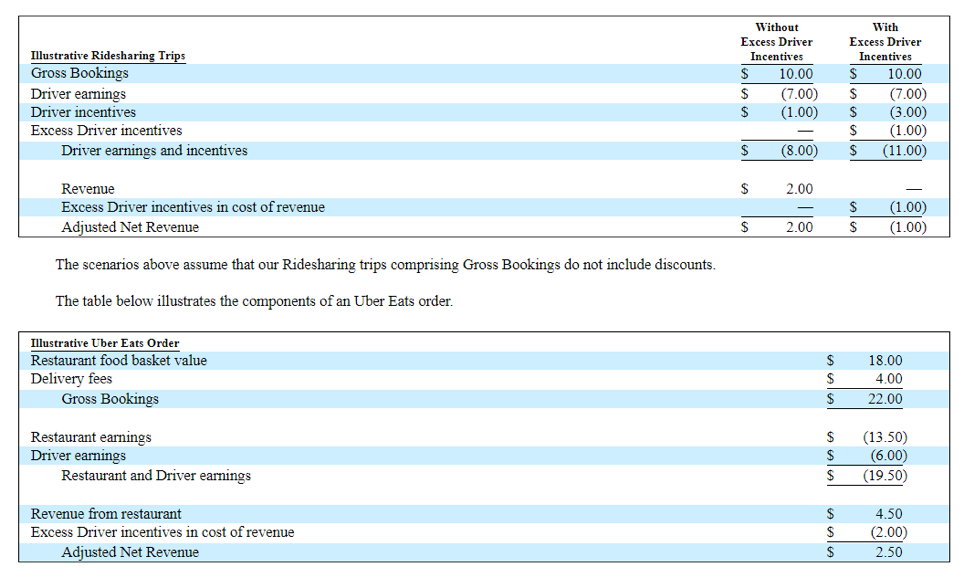

According to Uber’s SEC prospectus, the company posted losses from operations of $3 billion in 2016, $4.1 billion in 2017 and $3 billion last year. (Net income was actually $997 million in 2018 but it included one-time investment gains.) Uber said it expects operating expenses to increase “significantly” for the “foreseeable future,” warning that “we may not achieve profitability.” Uber’s compensation is dented heavily by its incentives. For example, if a trip costs the rider $10, the driver gets $7 plus another $1 in Uber incentives. Uber gets $2. If Uber ramps up its incentives to $4, it actually loses $1 on a $10 trip, according to the filing.

Source: Uber S-1/A filing, U.S. Securities and Exchange Commission

What gets investors excited is its market dominance and revenue growth. From 2016 to 2018, revenue nearly tripled from $3.84 billion to $11.27 billion. Gross bookings, or the total value of trips and not just Uber’s cut, more than doubled from $19.2 billion to $49.8 billion in 2016 to 2018. Such fast growth in an industry Uber created — after founders Travis Kalanick and Garrett Camp famously could not get a cab in Paris 11 years ago — and still dominates has attracted venture capitalists since the beginning.

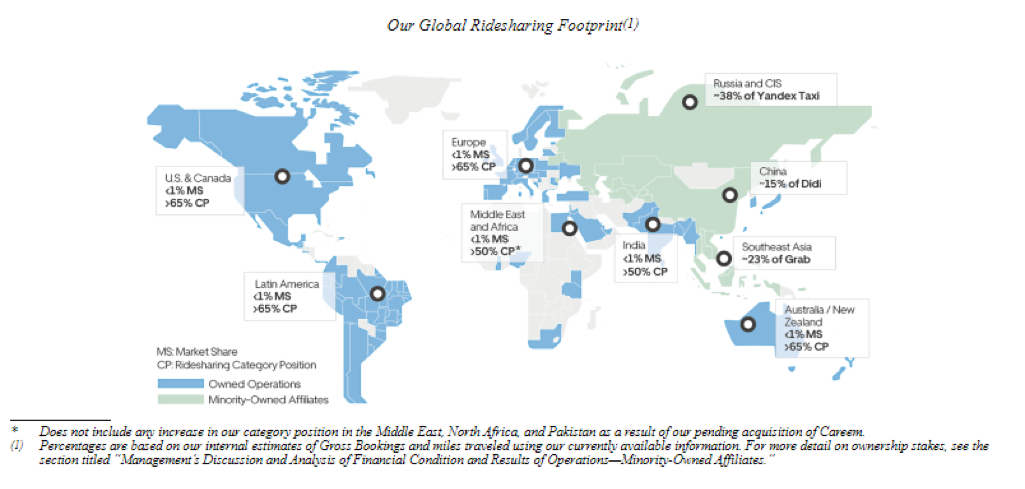

While Uber faces tough competition — such as from Lyft in the U.S., Didi in China and Grab in Southeast Asia (it took stakes in the latter two after they beat it back in their cities) — none so far can match its scale. “The ridesharing industry has become one of the most transformational growth sectors of the global consumer markets over the past five years with Uber establishing itself as the clear No. 1 player and in our opinion is paving a similar road to what Amazon did to transform retail/commerce and Facebook did for social media,” according to a May 1 analysts’ report from Wedbush Securities, where the stock has an ‘outperform’ rating.

Such giddy expectations have led to rumblings that Uber could achieve a $100 billion valuation at its IPO. Instead, it came in at around $82 billion on its May 10 debut. But even with a lower valuation, is it still too high given Uber’s losses? While the market is the ultimate judge, “I think it is well valued,” said David Erickson, Wharton lecturer and former co-head of global equity capital markets at Barclays, on the Knowledge at Wharton show on SiriusXM. Uber is “one of the transformative technology companies, and probably the most significant IPO we have seen in the market since Alibaba went public in 2014.”

“One thing we know about this market is there’s really no winner takes all. It’s not even winner takes most.”–Gad Allon

“Just because it is $80 [billion], $90 billion today doesn’t mean there isn’t significant upside if you look forward,” Erickson continued. He cited the case of Alibaba, which went public at $68 and recently traded at $173 a share. Five years ago, Amazon was trading at $331 a share with a $153 billion market cap. Today, Amazon trades around $1,835 a share with a $900 billion market value. “So obviously, they have done quite well even at that size.” Wall Street, he said, sees Uber as part of an elite group of tech companies that include Amazon, Facebook, Google and Netflix.

Uber operates in more than 700 cities in 63 countries and six continents, enabling more than 10 billion trips globally. Since 2015, its drivers have earned $78 billion, plus tips. In the fourth quarter of 2018, Uber served 91 million monthly active platform consumers (MAPC) and partnered with 3.9 million drivers. Uber sees future opportunities for growth since its rides only account for less than 1% of all miles driven globally. In countries it operates, only 2% of the 4.1 billion people there have used Uber.

Source: Uber S-1/A filing, U.S. Securities and Exchange Commission

A Different Uber

People today know Uber chiefly as a ride-hailing company: Riders use a smartphone app to hail drivers who use their own cars as taxis. But the future Uber is likely to be much different, according to Allon. “If I thought the end of the story is cars driving us from point A to point B, that might be very short-term success. In the next few years, it’s going to be hard to make that profitable,” he said. But since it also offers meal delivery, freight, electric bikes and scooters, self-driving vehicles and urban aviation, “Uber is going to turn out to be quite different than what they are now.”

Allon said ride-hailing is akin to a “loss leader” for Uber as a way to create a “network effect that piece by piece will be replaced by other elements” once the technology and market are ready. He cited the case of Netflix, which wanted to offer video streaming but the right technology was not yet in place. So they rented out DVDs by mail. “Shipping DVDs is not a great business” because they scratch easily and don’t last long and there are delivery costs, “but it allowed them to be in every household,” Allon said.

Uber’s platform and network effect buttress the stock’s bull case because it lets the company pivot into other markets. “A core tenet of our bull thesis on Uber is around the company’s ability to morph its unrivaled ridesharing platform into a broader consumer engine with Uber Eats, Uber Freight and autonomous initiatives ‘just scratching the surface’ of the full monetization potential of this platform over the next decade,” the Wedbush report said. Saying Uber is just a ridesharing platform “would be undervaluing the value of the entire company, which has the DNA to become a game changing consumer distribution ecosystem.”

What’s more is that Uber and other ride-hailing services are protected by “huge” barriers to entry in their business, said Evan Rawley, professor of strategic management and entrepreneurship at the University of Minnesota, on the radio show. “There is a huge ‘chicken or the egg’ problem here, which creates … a major barrier to entry” for new entrants, he said. “You are never going to get a rider to click your app if you don’t have any drivers, and you are never going to get drivers if you don’t have riders.”

“Just because it is $80 [billion], $90 billion today doesn’t mean there isn’t significant upside if you look forward.”–David Erickson

Bertrand Competition

At some point, though, Uber must turn a profit to stay in investors’ good graces for the long haul. Will investors have the patience to wait? Erickson said shareholders might be willing to give enough rope to a transformative company such as Uber. He cited the case of Amazon, which went public in 1997 but didn’t become profitable until 12 years later. “Uber is one of those companies [that investors will give] a significant amount of rope … to execute their plan,” Erickson said, adding that it helps that the company took in more than $11 billion in 2018 revenue and has about $16 billion in cash and cash equivalents after the IPO.

Rawley is not so sanguine. “Uber is losing so much money … that they really need to think about ways to generate positive cash flow in the future,” he said. A major problem is that the “core business is essentially an undifferentiated product.” It is not so different to take Uber or, say, Lyft. That means the two have to compete on price, in the absence of collusion. “If there is even one other competitor in an undifferentiated market, there is high potential for prices to drop down to marginal costs. If prices are at marginal costs, there is no profit,” said Rawley, describing the economic model known as ‘Bertrand Competition.’ “All businesses need to generate profits to be worth something in the future.”

Like Uber, Lyft has also booked years of losses. According to its prospectus, operating losses were $692.6 million in 2016, $708.3 million in 2017 and $977.7 million last year. Lyft also warned that it “may not be able to achieve or maintain profitability.” However, revenue jumped from $343.3 million to $2.16 billion in the same period. Today, shares of Lyft are down by a third from its IPO price of $72 to about $50. But despite their similarities, Uber and Lyft differ in one key area. “Uber is really trying to be a global transportation platform company, whereas Lyft is more focused on being a ride-sharing company here in the U.S.,” Erickson said.

Rawley credited Uber CEO Dara Khosrowshahi, who was hired in 2017, for instilling some discipline on spending. He said Uber used to spend about $20 million a month on its autonomous vehicle project, which was not even the core business. “[Khosrowshahi] has really refocused the organization around ride-hailing, and some more sensible corporate strategy investments such as the food delivery business, which is really complementary, as well as in some defensive expansions.” For example, it is getting into electric scooters and bikes as well as offering the Uber Bus in a bid to dominate transportation options.

Moreover, the CEO “has organized the businesses in such a way that there is a hope … that in the not too distant future Uber could actually be cash flow positive,” Rawley said. “And they are going to have to generate a lot of cash in the not too distant future to justify anything near a $90 billion valuation.” Right now, the path to profit is for Uber to raise fares or cut reimbursements to drivers, he said. “That is going to make people unhappy with them, and there’s going to be more regulatory scrutiny.”

“Uber is losing so much money … that they really need to think about ways to generate positive cash flow in the future.”–Evan Rawley

Rawley said Uber continues to face “a tremendous amount of regulatory risk” worldwide. If Uber and Lyft become duopolies in cities, it could lead to more local governments assessing fees on their services, further hurting the path to profitability. “Basically all of [Uber’s] cash flow is being generated by two businesses,” ride-hailing and food delivery, he said. “Those businesses are highly subject to local regulation.”

A Kinder, Gentler Uber?

Uber’s old attitude was to thumb its nose at regulators. But Khosrowshahi is taking a different path. He succeeded Kalanick after the company was hit with allegations of sexual harassment, faced lawsuits, hid a data breach from regulators, and upset drivers. It even created an app that blacklisted government officials posing as riders, according to The New York Times. Uber said the program denies riders who violate its terms of service, “whether that’s people aiming to physically harm drivers, competitors looking to disrupt our operations, or opponents who collude with officials on secret ‘stings’ meant to entrap drivers.”

Kalanick ran the company in a “much more entrepreneurial, seat of the pants style. Uber had anticipated that they would have such a big head start if they just rammed through their product in every local market, that they would essentially be a monopolist and they would be able to reap monopoly rent,” Rawley said. “That hasn’t been the case. They are challenged in every market that they are still operating in. … They have had to retreat from China and Southeast Asia under intense competition there.”

Rawley said that “Dara has had to significantly reorient the organization, professionalize the management, put in human resources systems that will conform to what is expected of a major public company operating on a global scale.” Uber’s prospectus sheds light on its new attitude, listing eight principles the company abides by, starting with ‘We do the right thing. Period.’ To curry favor with drivers, Uber set aside 5.4 million shares for qualified drivers to buy at the IPO price and will give a one-time reward ranging from $100 to $40,000 per person.

Notably, Uber does not have any ‘supervoting’ stock, which carry more votes per share and typically are held by founders and other insiders so they can exercise more control over their companies. (Facebook CEO Mark Zuckerberg, for example, holds Class B shares that each carry 10 votes.) Nine out of Uber’s 12 directors are independent. Kalanick, one of Uber’s biggest shareholders, and co-founder Camp are both directors but not in management.

Erickson compared Khosrowshahi’s hiring to Novell CEO Eric Schmidt joining Google in 2001 as chairman and later CEO, succeeding young co-founder Larry Page. Khosrowshahi, the former CEO of Expedia, is a “well-known, seasoned CEO with a significant track record in his own right,” he said. “That is one of the positives that a lot of institutional investors are taking comfort in.” Erickson also noted the addition of another veteran, Nelson Chai, as CFO. Chai had been the CFO of Merrill Lynch and New York Stock Exchange. (Chai sits on the board of overseers at the University of Pennsylvania’s School of Arts and Sciences.)

“Founder-CEOs are more mission-driven, are usually bolder and more confident in their ability to withstand sea changes in the market.”–Gad Allon

But there are distinct advantages to retaining a founder as CEO as opposed to a hired gun. “It makes a huge difference,” Allon said. “Founder-CEOs are more mission-driven, are usually bolder and more confident in their ability to withstand sea changes in the market.” He cited the case of Amazon’s Jeff Bezos. “To some extent, the board depends on Bezos more than Bezos depends on the board.” Everything else being equal, Allon added, the non-founder CEO is “traditionally a weaker CEO.”

Apple is a classic case. “We’ve not seen bold moves from [CEO] Tim Cook. He’s mostly what [venture capitalist Ben] Horowitz calls a ‘peacetime CEO’ rather than a ‘wartime CEO.’ He got a firm with a huge technological advantage, with a huge market advantage, a product that sells like hotcakes. He just needs to not mess around with the system and execute,” Allon said. “But it’s clear that until now, Apple has not been positioning itself for the next generation with its products. The iPhone … is more of the same. … We have not seen a new innovative product.”

To some extent, this is a concern with the current Uber CEO. “I’m not sure whether … he will be very innovative,” Allon continued. “That’s exactly the trap that many non-founder CEOs are in.” While there are many good non-founder CEOs and many founders who should not be CEOs, “one of the redeeming factors of being a founder-CEO is the ability to [beat the] odds,” he said. “Everybody told them [what they were attempting] was nonsense, and they still did it. … That level of credibility is very hard to replicate afterwards. Some people do … but it’s not easy.”

Innovation will be key to Uber staying on top — and expectations are high. Uber has the potential opportunity to join “this hallowed ground of other tech stalwarts such as Amazon, Apple, and Google over the next decade,” Wedbush analysts wrote in their report. “Uber is clearly one of the most transformational companies in the world as the company has essentially singlehandedly changed the nature of transportation worldwide.”