In the following article, Wharton finance professor Michael R. Roberts explains why some homeowners should consider investing any extra money they have rather than using it to make additional mortgage payments.

There is no shortage of articles and videos discussing the pros and cons of paying off your mortgage early. Some are quite confident in the view that paying off a mortgage as quickly as possible is unambiguously good. While there are psychological benefits of avoiding debt, the financial ones are less clear. Here I show data suggesting that many homeowners may be better off investing any extra money, as opposed to using that money to pay their mortgage off early.

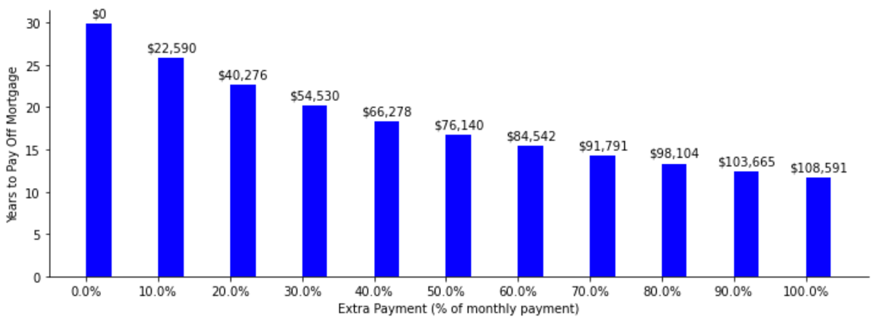

To make things concrete, consider a hypothetical homeowner, Lena, with a 30-year, 3.0% fixed-rate mortgage of $500,000. Her monthly mortgage payment is approximately $2,108. Figure 1 shows the interest savings and reduction in time to pay off the mortgage that occur when Lena pays more than her required monthly payment.

Figure 1: Present Value of Interest Savings and Years to Repay Mortgage

The figure shows the more Lena pays each month, the more quickly she pays off the mortgage (shorter bars) and the greater the interest savings (larger numbers on top of the bars). For example, paying 10% more each month allows Lena to pay off her mortgage in 26 years and save $22,590 in interest expense.[1]

Opportunity Cost and Taxes

Paying a mortgage off early comes with a cost; namely, the extra money used to pay down the mortgage cannot be used for other opportunities. Loosely speaking, if Lena could find an investment that offers a rate of return higher than the rate she pays on her mortgage, then she could invest any extra money, use the earnings from her investment to help pay off her mortgage, and still have money left over.

The “loosely speaking” caveat refers to tax considerations. Investment earnings are taxable and, depending on the nature of the earnings (e.g., income versus capital gains), taxable at different rates. However, another cost of paying off a mortgage early is higher taxes. Mortgage interest is tax deductible. For example, Lena’s first-year interest expense totals $14,857. At a personal tax rate of 24%, this implies tax savings of $3,566 in just the first year of the mortgage. In effect, the government is paying homeowners to take on debt. Paying a mortgage off early reduces the interest expense and the corresponding tax shield.

Investment Options

Because Lena has to pay her mortgage, or face significant financial repercussions, a risk-free investment of similar term is a natural alternative investment. The interest rates as of mid-February 2021 on long-term safe investments are all well below 3%, the cost of Lena’s mortgage. For example, the yield on the 30-year U.S. Treasury bond is 2.2%, and the yield on AAA-rated, long-term municipal bonds is 1.3%. Thus, any alternative investment worth considering will come with some risk. The question is: how much risk?

“While there are psychological benefits of avoiding debt, the financial ones are less clear.”

We can answer this question by imagining Lena has an extra $210 of income each month and is deciding what to do with the money. One option is to invest the money in a risky asset, like an exchange-traded fund (ETF) mimicking the Standard and Poor’s (S&P) 500 index, each month for the 30-year life of the mortgage. There are of course many other investment options, but a stock market index is illustrative. Another option is to use the money to make slightly larger mortgage payments. Because $210 is approximately 10% of her mortgage payment, Figure 1 above shows that the second strategy will reduce her 30-year mortgage by approximately four years and free up all of her income for savings from that point forward. Paying off a mortgage early shifts savings into the future.

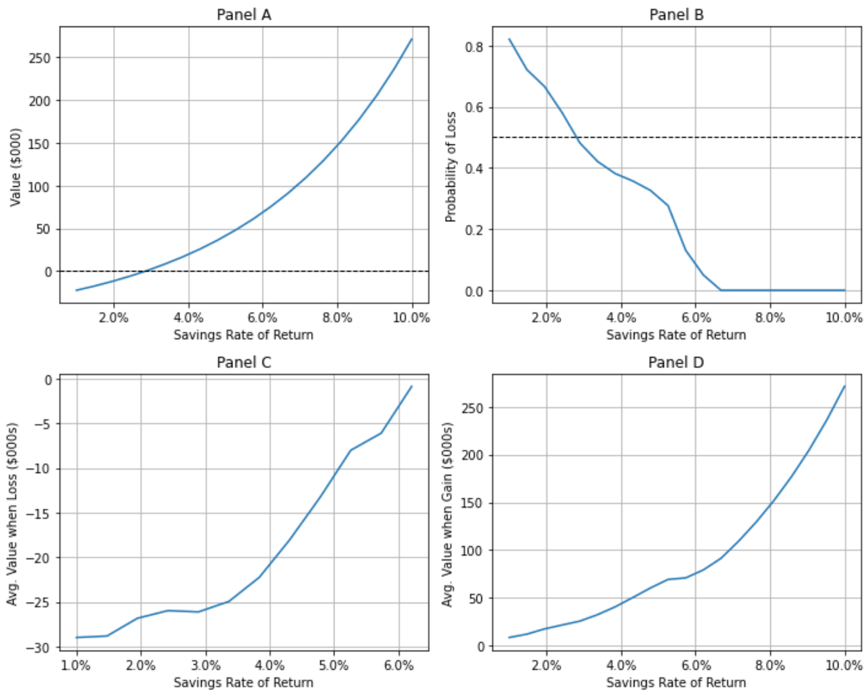

Which option is better? Put differently, which option will lead to more savings for Lena after 30 years? We can’t know for certain without knowing the future performance of the stock market. However, we can use the past as a guide. Figure 2 below contains four panels, A through D, illustrating Lena’s performance and risk exposure when investing in the stock market relative to paying off her mortgage early.[2] To evaluate her investment performance, we can take every 30-year window of realized monthly stock market returns over the last 100 years and apply them to Lena’s monthly savings. This process generates a distribution of savings outcomes for Lena after 30 years, against which we can compare the outcomes from a savings strategy resulting from her paying off her mortgage early.

The concern with this exercise is its reliance on past returns. With interest rates near zero, significant economic growth is needed to generate market returns close to those experienced over the last 100 years – approximately 11% per annum. To explore the implications of different future investment performance, let’s repeat the process above by reducing the average return of historical stock returns while maintaining the same risk (i.e., volatility).

Panel A shows that as the return on Lena’s savings increases, i.e., we move from left to right along the horizontal axis, the value of investing the money relative to paying off the mortgage early increases. At a 3% savings return, the cost of her mortgage, Lena would be indifferent between saving extra money and paying down her mortgage early because both options lead to similar average savings balances after 30 years. Savings rates higher (lower) than 3% lead to higher (lower) savings for Lena if she invests her money as opposed to paying down her mortgage early. For example, a 5.5% average return on savings, half that of the historical return, leads to an extra $57,000 in after-tax savings if Lena invests the $210 per month as opposed to using it to pay down her mortgage more quickly.

Figure 2: Performance and Risk of Investing vs. Paying Mortgage Early

Panel B illustrates the relative risk of the investment strategy. When the return on savings is 3%, the same as the cost of the mortgage, the choice between investing the money and paying down the mortgage comes down to a coin flip; there is a 50-50 chance that either option will lead to a better outcome. However, if future average market returns are 5.5%, for example, the probability that investing extra money leads to less savings than paying down the mortgage early is only 26%. For average returns above 6.5%, the probability that investing the extra money is a bad choice is zero. In other words, there hasn’t been a 30-year historical period in which the average stock market return was below 3%, even when the average return for the 100-year period was only 6.5%.

As important as understanding the likelihood of a strategy going wrong, Panel C shows how much money can be lost when it does. When the investing strategy performs poorly relative to paying the mortgage off early, Lena can expect to have $7,000 less in her savings account after 30 years if the average return on her savings is 5.5%. Her total expected savings at the end of 30 years is $318,000, implying the loss is just over 2% of her total savings. If the average market return in the future is only 1% per annum, Lena can expect to lose $27,000, or 8.5% of her savings, relative to what she would have had she paid down her mortgage early.

In contrast, Panel D shows that if investing outperforms paying off the mortgage early, Lena can expect to have $70,000 more in her savings account after 30 years when the average return is 5.5%. Panels C and D illustrate an interesting asymmetry; losses when the investment strategy doesn’t perform well are small relative to the gains when it does.

Additional Considerations

Other considerations point to the benefits of investing extra money as opposed to paying a mortgage off early. Tying up savings in an illiquid asset like a house is problematic when you need money. For homeowners with higher income tax rates, the tax savings from a mortgage are even larger, as long as the mortgage principal is under the federal cap of $750,000 or $1 million for mortgages originated prior to 2017. There are also alternative investments (e.g., fixed income) available to investors that are less risky than the stock market but still offer potentially greater average returns than the cost of a mortgage. There are even some psychological arguments for maintaining a mortgage.

All that said, perhaps the stock market going forward will return significantly less than 5.5%, which while convenient was chosen primarily to ground the discussion. Japan over the last 30 years is a good example of persistently low – approximately 1% per annum – stock returns. Perhaps Congress will eliminate the tax-deductibility of mortgage interest or raise the capital gains tax. Anything is possible, so redirecting money from your mortgage to a risky investment is…risky. Further, if your investment horizon is significantly shorter than 30 years, e.g., 10 years, the risk profile can be quite different from that discussed here. Related, older homeowners, those nearing or in retirement, may have less appetite for risk.

Ultimately, paying off your mortgage early is not necessarily a financially wise decision for everyone; making an informed decision is.

Michael R. Roberts is the William H. Lawrence Professor of Finance at the Wharton School of the University of Pennsylvania.

***

[1]Interest savings are measured in present value terms because a dollar received today is worth more than a dollar received 30 years from today. Money received today can be invested today; money received later cannot.

[2] I assume that Lena invests an amount equal to 10% of her monthly mortgage, $2,108, in a total U.S. stock market index each month, her income is taxed at 24%, and she faces capital gains taxes of 20% on any investment earnings at the end of the 30-year period.