![]()

In the first article of a series that will be published over the coming year, authors Barry Libert, Megan Beck and Jerry (Yoram) Wind explore why companies whose business models involve leveraging networks generate more value than traditional firms. Libert is CEO of OpenMatters and Beck is the chief insights officer. Wind is a Wharton marketing professor and also director of Wharton’s SEI Center for Advanced Studies in Management. They also wrote a book called The Network Imperative: How to Survive and Grow in the Age of Digital Business Models. The authors would like to thank LiquidHub for sponsoring the research that informs this series.

* * *

“Society is undergoing tremendous change right now — the sharing and collaboration practices of the Internet are extending to transportation (Uber), hotels (Airbnb), financing (Kickstarter, LendingClub) and music services (Spotify). The rise of the collaborative economy, of which the Open Source community is a part, should be a powerful message for the business community. It is the established, proprietary vendors whose business models are at risk, and not the other way around.”

— Dries Buytaert, Founder of Drupal

Klaus Schwab, founder and executive chairman of the World Economic Forum, stated earlier this year that he believes we are experiencing the fourth industrial revolution. This is a revolution of networks, platforms, people, and digital technology that is “blurring the lines between physical, digital and biological spheres.” Our research supports this theory. We believe that digital networks are the key differentiator, which tie together these spheres in a way that enables new forms of sharing, distributed intelligence and value creation.

This revolution marks a critical inflection point. We are navigating great, worldwide shifts from physical to digital, closed-source to open-source and linear to exponential. New forms of assets (intangibles) and new ways of doing business (networks) mean that the formal frameworks and foundations used globally to design, measure and value organizations by investors, leaders, regulators, economists and accountants are increasingly inadequate and misleading, leading to the misallocation of limited human and financial resources.

A few leaders and investors saw this shift coming and have benefited greatly — just look at the unicorns. But most leaders and investors were not so prescient. It’s now time for all business leaders, economists, educators and investors to recalibrate and adjust — and quickly. Funding, investors, customers and talent are all flowing towards digital networks.

“Physical things do not scale quickly, easily or cost effectively. Building the U.S. interstate highway system took 35 years and an estimated $425 billion…. Facebook grew to 500 million users in a little more than six years.”

We have spent the last decade researching this shift. Our book on the topic, The Network Imperative, will be published in June. This series of articles with Knowledge at Wharton approaches the shift from a different angle, by examining how digital networks, technology platforms and network-based business models are affecting all industries.

Meeting the Challenge of Networks

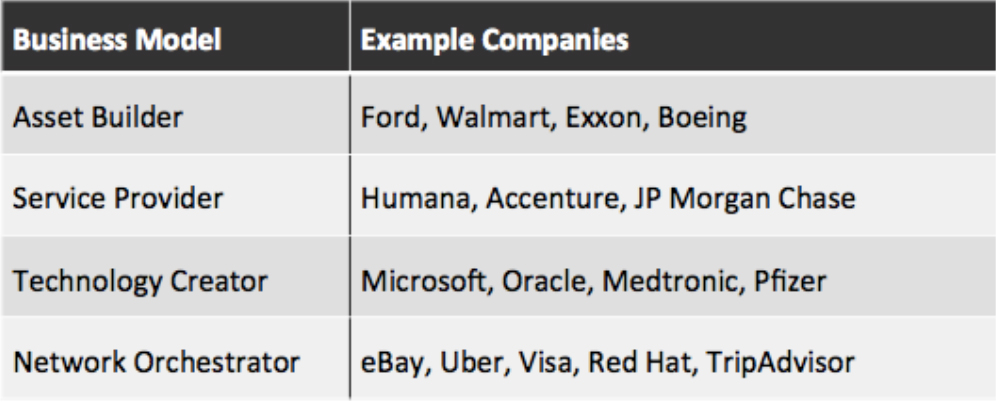

Our insights are based on the simple premise that different business models, based on different types of assets and technologies, create different economic outcomes. We identified four business models, each with its own value proposition:

- Asset builders deliver value through the use of physical goods (physical capital). These companies make, market, distribute, sell and lease physical things.

- Service providers deliver value through skilled people (human capital). These companies hire and develop workers who provide services to customers for which they charge.

- Technology creators deliver value through ideas (intellectual capital). These companies develop and sell intellectual property, such as software, analytics, pharmaceuticals and biotechnology.

- Network orchestrators deliver value through relationships (network capital). These companies create a platform that participants use to interact or transact with the many other members of the network. They may sell products, build relationships, share advice, give reviews, collaborate and more.

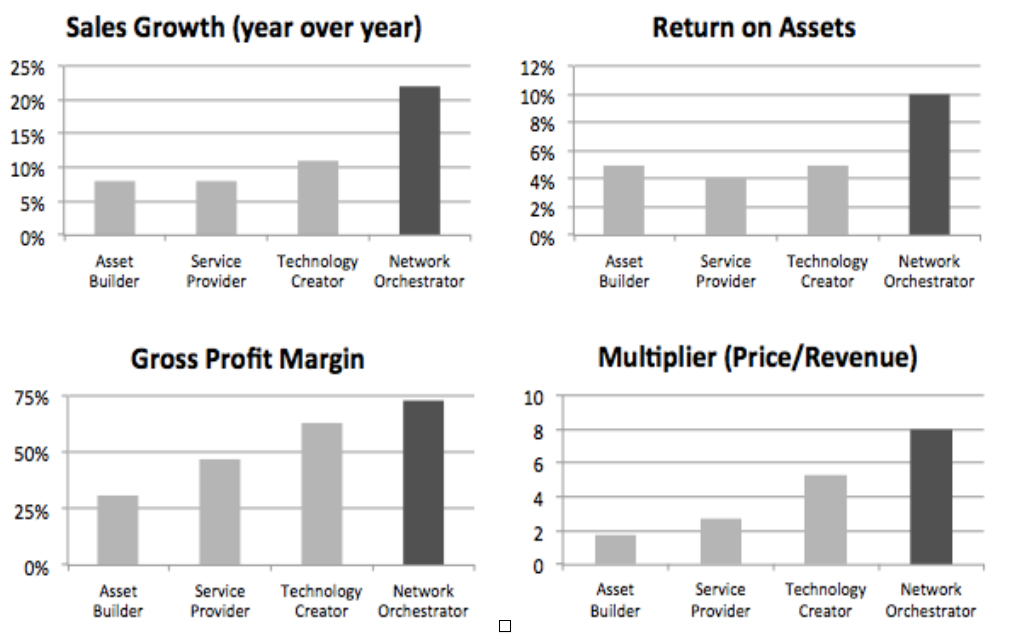

Knowledge at Wharton readers may recall this business model framework from a previous article published in 2014. When we applied this framework to the S&P 1500 Index (a mix of small-, mid-, and large-capitalization companies), we observed that companies using these business models were not equal.

As we had noted back then, there were clear and dramatic differences in performance. By leveraging technology and the network effect, network orchestrators outperformed the rest. Network orchestrators, on average, grew revenues faster, generated higher profit margins, and used assets more efficiently than companies using the other three business models. These advantages resulted in remarkably higher enterprise values when compared with revenues.

The reasons are intuitive. Physical things do not scale quickly, easily or cost effectively. Building the U.S. interstate highway system took 35 years and an estimated $425 billion (in 2006 dollars). In contrast, Facebook grew to 500 million users in a little more than six years. Digital technology and networks make all the difference.

Not only are many of the most valuable goods in our market — such as ideas, intellectual capital, and access — digitizable, but also our digital networks allow them to proliferate with great ease. The scaling cost is close to zero. When you add the network effect, where each additional participant (or node) in the network increases the value for every other participant, the network drives its own growth.

However, few organizations have adjusted their business model in light of the new possibilities — probably because changing an organization’s business model is difficult. Each business model is the outcome of capital investments in one of the four asset types — physical, human, intellectual or relationship capital. Leaders must reallocate funds to create business model change, but most leaders are held captive by outdated mental models. Most of today’s business leaders honed their skills in the industrial age, and have difficulty shifting away from physical assets towards digital network assets.

The companies that have truly built network-orchestrating organizations don’t just do one thing differently; they do everything differently — from leadership to recruiting to production to advertising.

When we share this research with executives and board members, most intuitively understand the implications for their organizations. The common refrain, however, is: “How can my team and I make use of this information and become a networked organization using today’s digital platforms, since our organization didn’t start out as a network?”

It is certainly true that new ventures such as Airbnb, Uber, Facebook and Pinterest were born with a radically different worldview, and their lack of legacy has been an advantage in creating this new, industry-beating business model. But we also know that every organization has the assets — people and data — to create powerful network-based business models. They just need to change their mental model and bring their currently dormant and underutilized networks to the center of their organizations. To help them do that, we have identified ten principles that clarify how network orchestrators operate differently, based on our research and experience advising firms.

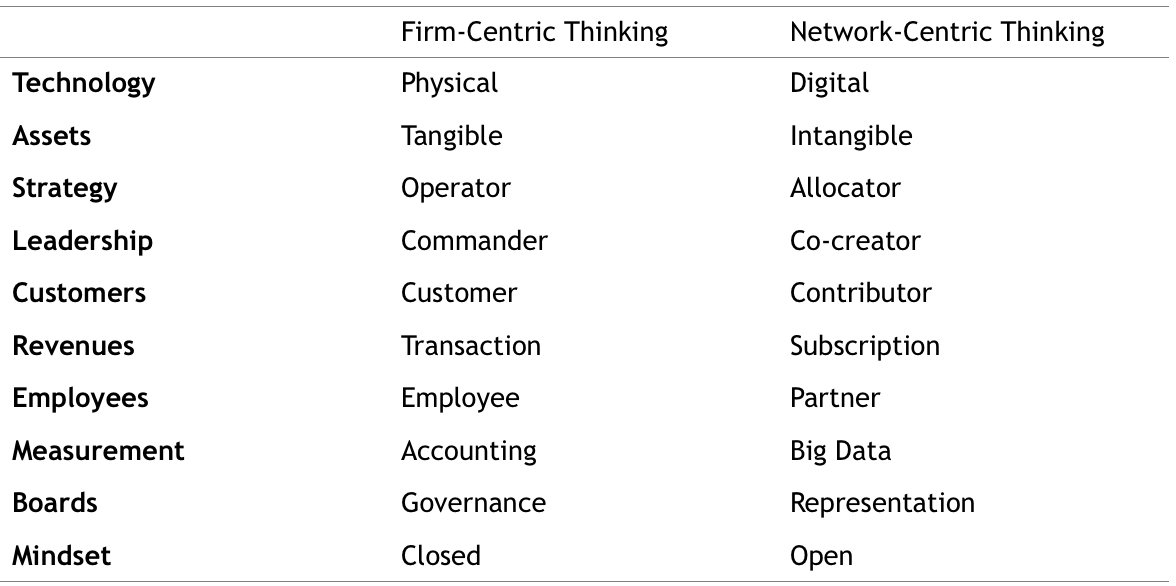

Network-vs. Firm-Centric Thinking

Each of these principles is a lever that organizations can use, and are using, to transform their business models and their industries around them. As we examine different industries in this series, we will see how these principles have come to life in different ways. But despite their industry-transforming influence, network orchestrators are still far and few between. By our estimates they make up only 2% of publicly traded companies. For the rest, network orchestration is still uncharted territory.

Network Proliferation in Every Industry, Every Function

We are all learning what this new world of networks means. Networks are large, many-faceted, and rapidly evolving. The companies that have truly built network-orchestrating organizations don’t just do one thing differently; they do everything differently — from leadership to recruiting to production to advertising. And networks have evolved differently in different industries — from transaction platforms like Apple Pay and Paypal to marketplaces like Etsy and Ebay to social platforms like Facebook and LinkedIn. Even further, networks are crossing traditional industry and geographic bounds, making our traditional ways of looking at the market obsolete.

Examination of each network organization reveals some insights, but you have to step back for the wider view in order to start grasping the implications and influence of networks on the market. We hope that as this series gathers experts from many disciplines and probes this phenomenon from many angles, you will be able to see the full picture and illuminate the true nature of these networks and their implications for business. Specifically, over the coming months we will look at how the network revolution is affecting the following industries: real estate, automotive, finance, health care, industrial, education, publishing, transportation and logistics, advertising, public relations and marketing, sports and entertainment.

“Networked business models unlock greater growth, revenue, profit, and value, but achieving them requires existing leaders to adapt not only what they do, but also how they think….”

The implications for organizations — be they for profit or not, large or small — are significant. Networked business models unlock greater growth, revenue, profit, and value, but achieving them requires existing leaders to adapt not only what they do, but also how they think, in order to adapt their people, processes, products and technologies to the network world. Shifting away from your deeply ingrained industry and organizational mental models is a very difficult and important issue that this column will explore. We will address not just the why, better value, growth and profits, but also what to do and how to get started.

We hope this column will help you put the changes that are playing out in the structure of the global economy into a context that helps you survive and thrive. We also invite you to add your own comments and stories in the comments section below. Tell us your stories, experiments, pitfalls, and obstacles, and we can all learn together. We hope that you will join us on this journey, read along and share your own stories. We know it will be worthwhile for all involved as we reshape the world together.