In the following article, Wharton finance professor Michael R. Roberts explains the value of shopping for a mortgage and clarifies the trade-offs homebuyers need to weigh when there is no obvious choice.

Many websites are clear on the importance of shopping for a mortgage, as well as providing tips on how to do so.[1] What is often less clear is the actual value of shopping and, more importantly, how to select among mortgages in which there is no obvious winner. The goal of this article is to quantify the potential savings from shopping and the trade-offs homebuyers should consider in choosing among certain mortgages.

To ground the discussion, consider a homebuyer purchasing a home for $750,000. The buyer has $250,000 for the down payment and pays the remainder with a $500,000, 30-year, fixed-rate mortgage – the most popular residential mortgage in the U.S. According to Reuters, this loan amount is substantially larger than the average U.S. mortgage of $354,500, but less so for the Southeastern Pennsylvania region on which we are focused.

As of March 19, 2021, Bankrate.com provided approximately 100 mortgage estimates from different lenders for our homebuyer’s ZIP code. The estimates covered credit scores ranging from 660 to over 740. While diverse, the data come with a host of obvious limitations, yet remain illustrative for the purposes of this article.

The Savings

The Consumer Financial Protection Bureau (CFPB) estimates that the average homebuyer spends $300 more per year on their mortgage as a result of not shopping for the least expensive alternative. Table 1 below highlights that this average masks a great deal of variability in the data, particularly for larger mortgages.

For each credit rating category, three estimates are presented. Each estimate is computed as the difference between the most and least expensive loans in a credit score group. The total cost is computed as the present value of all mortgage payments and upfront costs (points and broker/lender fees), if any, over the 30-year term. The five-year cost is similar but computed over the first five years of the loan. Five years is an approximation of the typical “life” of a mortgage, given the frequency with which homeowners refinance their mortgages or move. The last column shows the difference in the monthly mortgage payments.

The cost differentials are large. Over the full 30-year life of the loan, choosing the “right” mortgage leads to savings around $50,000 in today’s terms. Even over the effective term of five years, the savings are over $10,000. Per month, some homebuyers can save over $300. While these estimates represent the maximal cost savings and perhaps not those experienced by every homebuyer, they emphasize just how valuable mortgage shopping can be.

Table 1: Cost Savings on Mortgages by Credit Score

| Difference Between Highest and Lowest

Cost Mortgages ($) |

|||

| Credit Score Range | Total Cost* | 5-Year Cost* | Monthly Payment |

| 720-740 | 50,066 | 10,974 | 270 |

| 700-720 | 49,036 | 14,088 | 270 |

| 680-700 | 56,875 | 12,495 | 305 |

| 660-680 | 48,915 | 10,564 | 272 |

* Total Cost and 5-Year Cost figures are present values.

Narrowing the Field

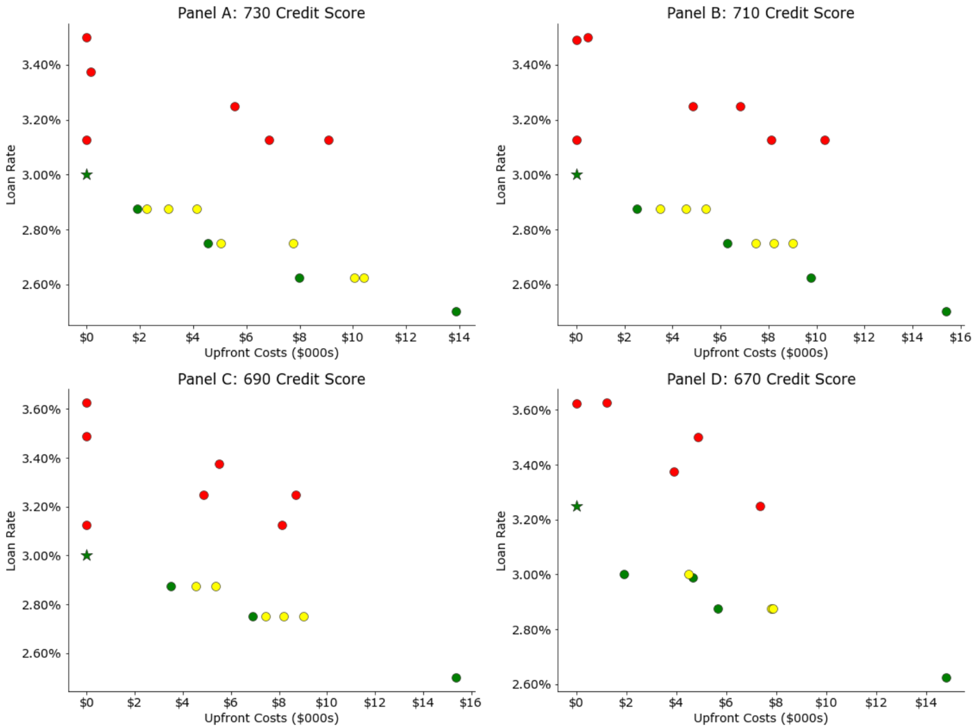

After obtaining quotes, how should homebuyers choose among the different mortgage options? Figure 1 helps answer this question. The panels contain similar information for different groups of mortgage quotes based on homebuyers’ credit scores, which are indicated at the top of each panel.

Each point in a panel corresponds to a single mortgage quote consisting of a rate (vertical axis) and upfront cost (horizontal axis). Moving northeast in each panel corresponds to more expensive loans – higher rates and upfront costs. Moving southwest corresponds to less expensive loans – lower rates and upfront costs.

“Ultimately, the final challenge confronting homebuyers in choosing a mortgage is determining how long they anticipate staying in their current mortgage … assuming they have the cash to pay any upfront costs.”

The red dots are mortgages that are easily dismissed as financially bad options. Why? Because every red dot has an interest rate and upfront cost combination that makes it strictly worse than the lowest rate with no upfront costs (the green star). A homeowner should never choose a loan, with or without upfront costs, that has a higher rate than a loan without upfront costs.[2]

The yellow dots are also financially bad options. These mortgages offer a lower rate than the lowest-rate mortgage with no upfront costs, but there are other mortgages with identical rates and lower upfront costs. In other words, for each yellow dot, we can move westward to find another mortgage that offers the same rate but lower upfront cost – the green dots.

Figure 1: Mortgage options by Credit Score

Picking a Winner

The green dots (and green star) are the finalists of our mortgage tournament and, unfortunately, there is no obvious winner. Lower rates are accompanied by higher upfront costs. That is, there is a trade-off: pay more now, or pay more later. Given people’s biases towards the near term, having to spend even more money when closing on a house is often unappealing, if not impossible when homebuyers are strapped for cash at closing. Nonetheless, the question remains: How long does our example homebuyer have to remain in the mortgage to recover any upfront costs?

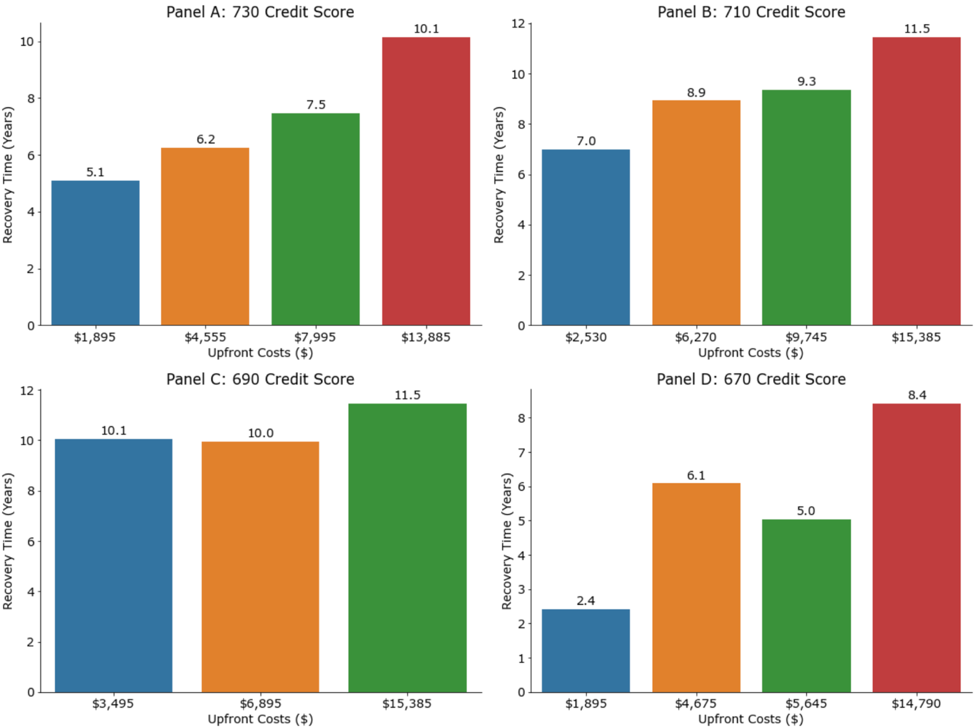

Figure 2 answers this question. Each panel presents the time to recover the upfront costs for each mortgage finalist. Focusing on Panel A in the upper left corner, the time to recover the upfront cost varies from approximately five to 10 years when the homebuyer has a credit score between 720 and 740 (i.e., the “730” group). The larger the upfront cost, the longer the stay required to capture the benefits of lower monthly payments.

Figure 2: Upfront Cost Recovery Times by Credit Score

In general, larger upfront costs coincide with longer recovery periods. However, the bottom two panels, C and D, show that this is not always the case. Depending on just how much lower the mortgage rate is when accompanied by upfront costs, there can be instances in which larger upfront costs are met with shorter recovery times.

Ultimately, the final challenge confronting homebuyers in choosing a mortgage is determining how long they anticipate staying in their current mortgage (i.e., not moving or refinancing), assuming they have the cash to pay any upfront costs. Needless to say, knowing when either event will occur with any certainty is difficult. However, refinancing risk is arguably relatively low in the current interest rate environment, so time in the home may be a more important consideration now. Thus, considering your timeline in the home in light of the time to recover any upfront fees can save you quite a bit of money either today or in the future.

Michael R. Roberts is the William H. Lawrence Professor of Finance at the Wharton School of the University of Pennsylvania.

***

[1] Private websites include Bankrate.com and nerdwallet, public websites including the Federal Reserve Board and the Federal Trade Commission.

[2] One does have to take care with other fees and optionality contained in loans, such as prepayment penalties. Further, some loans offer negative points or rebates, in which case the higher mortgage rate may be justified. Absent these exceptions, the conclusion stands.