For traditional accountants,

What explains this massive mismatch? More and more observers have recognized in recent years that a big part of a company’s true value depends upon intangible factors such as organizational knowledge, customer satisfaction, product innovation and employee morale, rather than on physical assets like machinery or real estate. While companies recognize the importance of these intangible factors, understanding and measuring their role in value creation poses a formidable challenge. Human resources departments may know how to tabulate payroll for a certain plant, for instance, but if asked to measure the motivation of its employees, they would probably be on uncertain ground. And yet, employee motivation and turnover are as crucial to that plant’s profitability as the size of its payroll.

To investigate such issues and more, the Wharton Research Program on Value Creation in Organizations has been conducting a series of studies on the key drivers of value creation jointly with Ernst & Young’s Center for Business Innovation. David F. Larcker and Christopher D. Ittner, co-directors of the Wharton program, explain that their research has three objectives. "First, we want to understand the value drivers in this economy," they say. "Secondly, we want to know how companies use these drivers for the design of performance evaluations, design of compensation plans and capital allocation plans. And finally, we want to examine what impact the identification of these value drivers should have on external disclosure."

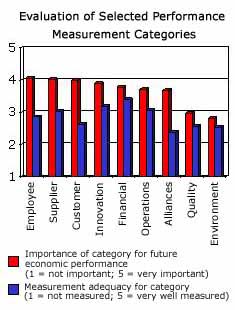

The results are now in from the first phase of a study carried out in conjunction with Forbes ASAP. This study asked corporate executives about key drivers of future economic value in their industries and also how well their organizations actually measure performance in these areas. Larcker and Ittner found that though companies have an idea about what factors are strategically significant to their future, they are doing a poor job of measuring performance in these areas.

There are exceptions, of course. For example, Larcker and Ittner discovered that companies attach high value to financial performance, and they are also doing a relatively good job of measuring it. One reason could be that businesses have been tracking such performance longer than they have been trying to monitor how they are doing in areas such as employee satisfaction. Still, despite the importance of financial performance, executives ranked four other areas as being more important for future value generation: Employee satisfaction, supplier performance, product innovation and customer satisfaction. The ability to manage alliances was seen as another crucial driver of future value. Quality and environmental performance, however, were less important than they might have been in the past. "Ten years ago, if you had asked, quality might have been No. 1," says Ittner, referring to the fact that total quality management was a hot topic back then. "Now that seems to have quieted down."

Signficantly, Larcker and Ittner found massive gaps between what executives believe are key drivers of future economic value and their organizations’ ability to measure performance in these areas. The biggest gap was in the customer category, which indicates that companies are still wrestling with ways to measure customer loyalty and satisfaction. Companies are also finding it tough to track how well they are managing alliances and fostering employee satisfaction, though executives believe that both these areas are crucial drivers of future value. "The way you manage your alliances is a much bigger deal now than it ever was, but there is nothing in today’s financial statements that says, here is how the company did," notes Larcker.

Larcker and Ittner believe that unless a company comes to grips with these issues, its performance measures will fail to support its strategic objectives. "If you don’t have good performance measures, it could screw up a good strategy," says Larcker. In addition, if companies do a good job of tracking their performance in these key areas, this could lead to more dependable disclosure of their future prospects. "If you disclose more, your cost of capital could go down because risk is reduced for investors," says Ittner. Serious efforts are now underway to see if greater corporate disclosure in these areas is essential since they offer sound leading indicators of a company’s future performance.

Having established the significance of these measurement gaps, Larcker and Ittner are now focusing on the next phase of their study. Their goal is to understand "how the choice of performance measurement systems affect organizational performance," they say. "In the first phase we just asked what is important for a company’s future performance and how well the company is measuring it. Now we want to look more closely at performance criteria and see what seems to work and what doesn’t. It is all part of the big value-creation puzzle." Churchill would probably agree that this puzzle is as mysterious and enigmatic as his Russian riddle.

Note to Readers:

Would you like to participate in a study about performance measures that predict economic success? Click here to participate in an on-line survey, or point your browser to www.valuecreationindex.com