The potential gains for the start-ups driving fintech (financial technology) are obvious. But the possibilities for extending financial services to the underserved – or those without services at all – are already being realized. With proper oversight and regulation even more is possible, notes this opinion piece by Kalin Anev Janse, secretary general and a member of the management board of the European Stability Mechanism (ESM), the Eurozone’s lender of last resort, and Gong Cheng, senior economist and policy strategist at the ESM. “It is thus essential for researchers and technical experts to shed light on the considerable social impact and promise fintech is offering and to find solutions to contain potential risks.”

Financial inclusion – making banking services accessible and affordable to everyone globally – has been a buzzword for the last few years. Technology-based financial services have propelled innovation to “bank the unbanked” making daily financial operations accessible and user friendly for almost everyone – especially people who had no access to banks before. Emerging markets like China, Kenya and Indonesia are leapfrogging the developed world. So – how is fintech making the world more inclusive?

We both have experienced first-hand the convenience that digitalised or mobile-based financial services have brought to our daily work and life.

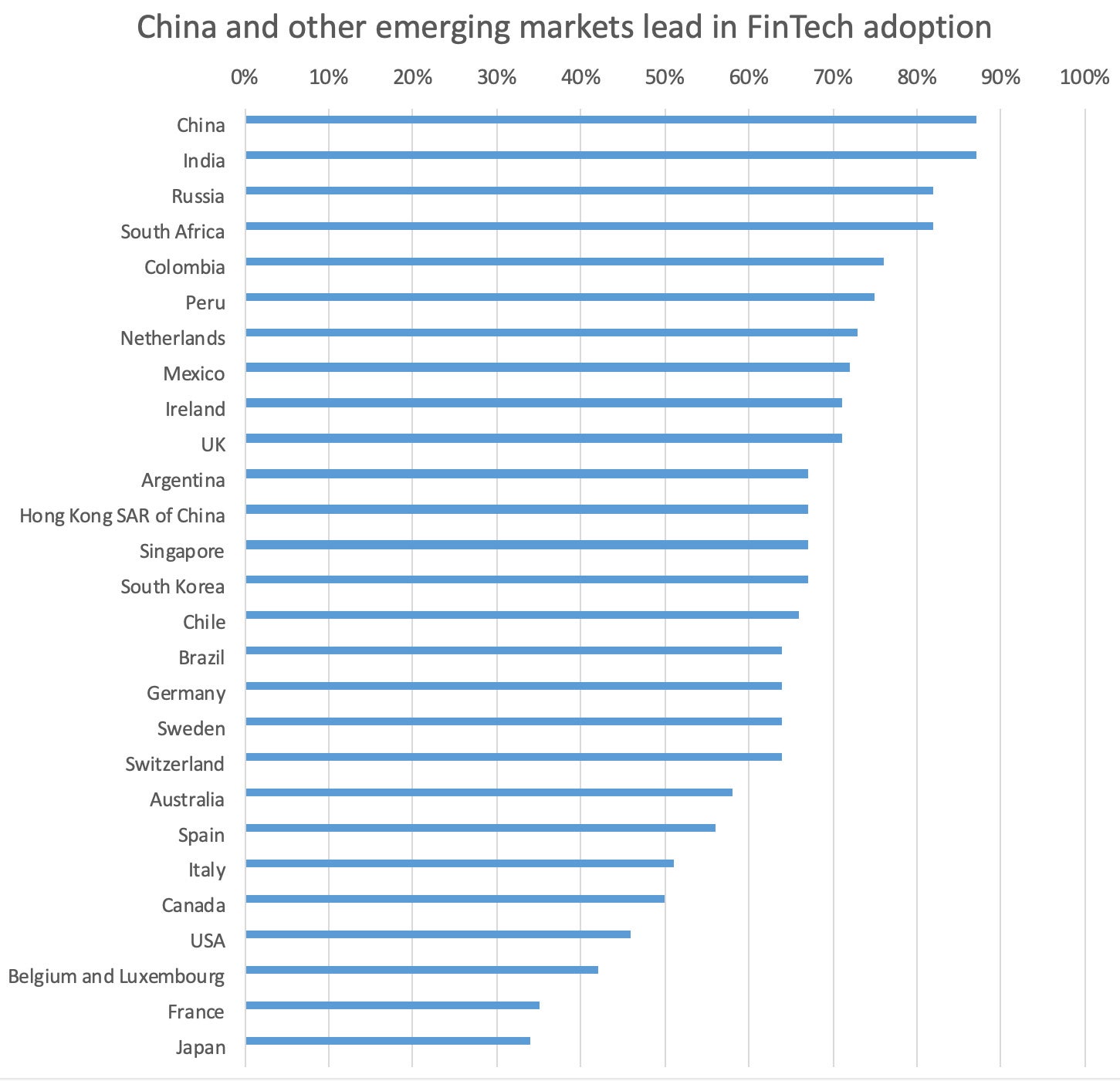

We are often in emerging markets. In China especially, we have been repeatedly surprised by the speed of fintech adoption. Mobile payment is widely used in China as an everyday payment method, from big modern malls down to the small food cart on the corner. When travelling to China, we use WeChat to order and pay a taxi or even a simple lunchbox (see pictures below). Local people in China can immediately tell that Gong is a Chinese living abroad, as he – from time to time – still uses the small banknotes and coins in his wallet long since discarded by locals.

Although fintech adoption is somewhat slower in Europe, a number of companies have started to penetrate certain market segments successfully. A few European “unicorns” have started to provide online payment and other banking services; there are upcoming European fintech companies (like Transferwise and Revolut) for example acting like an “Airbnb” for foreign exchange, offering customers spot exchange rates against minimum or no fees. So, Europe is stepping up its game.

The common theme across these few examples is that fintech innovation is lowering transaction and service costs and reaching a population that would otherwise be unable to benefit from standard financial services. In this op-ed, we present concrete examples of how fintech is making the world more financially inclusive.

Source: EY Global FinTech Adoption Index 2019; Notes: The figures show FinTech adopters as a percentage of the digitally active population in each market.

On Top of the Global Agenda: Financial Inclusion

Financial inclusion has been a recurring theme of financial sector reforms that the IMF and World Bank have advocated in financial assistance and macroeconomic consultations. Financial inclusion is especially important in emerging markets, like Asia, Africa and South America. It is a multifaceted concept that encourages access to formal financial services at affordable costs that can boost an economy’s overall growth and welfare. Often those targeted – families and small- and mid-sized companies – have either no or only very limited access to financial services.

To speed financial inclusion, the World Bank and the IMF launched the Bali Fintech Agenda in October 2018 during their annual meetings. The Agenda comprises 12 high-level principles to guide member states in elaborating appropriate policies to harness the benefits of what fintech can offer to bank the unbanked while mitigating any inherent risks. In her agenda-launching speech, IMF managing director Christine Lagarde estimated that 1.7 billion adults worldwide are currently deprived of access to financial services and fintech’s recognised comparative advantages is filling in the gap that traditional financial institutions could not.

Financial innovation propelled by fintech plays a key role in bolstering financial inclusion and makes simple financial instruments accessible. Two examples highlight the power and benefits of fintech, its role in enabling access to credit for small- and medium-sized enterprises (SMEs) as well as in reducing households’ financial transaction costs.

Fintech Provides Trade Credit to SMEs

In emerging markets, we often see economic distortions created by domestic financial market underdevelopment, especially credit market frictions. This is more prominent in fast-growing emerging market economies, such as China, where certain types of firms – mostly private – face credit constraint in the formal financial sector because of exorbitantly high costs or a credit rationing bias towards larger, state-owned enterprises. Small businesses, therefore, find it difficult to access trade credit, which plays an essential role in businesses’ daily operations and represents a large proportion of all trade transactions. The trade credit market has tightened even further since the global financial crisis, given that provision is falling in emerging markets.

“Financial innovation propelled by fintech plays a key role in bolstering financial inclusion and makes simple financial instruments accessible.”

In recent years, fintech companies have played an important role in complementing the formal banking sector and providing trade credit to small firms. Chinese mobile and online payment platform Alipay, for example, has since 2006 provided credit to vendors operating on the Chinese e- commerce platform, Alibaba. Alipay, and subsequently Ant Financial, developed an algorithm-based internal rating system taking data from vendors’ real-time transactions on commercial platforms, such as the Chinese online shopping website Taobao, to provide credit facilities.

Three key features show how Alipay/Ant Financial credit to SMEs helps to alleviate credit market frictions in China. First, using the data and information Alibaba has on its 16 million merchants, Ant Financial reduces information asymmetry between itself and potential borrowers, allowing it to extend credit to firms that traditional banks will not help due to information scarcity. This is especially important for start-ups, because they are unable to show the long record of business operations needed to be eligible for bank credit. For Ant Financial as a creditor, the information available enables a more accurate risk pricing, as it can tailor financial terms to the risk profiles of individual firms.

Second, Ant Financial has also developed savings instruments that pool spare money from Taobao – a Chinese online shopping website users — and channel it to the firms in need. When Yu’ebao was launched as a money market fund in 2013, the interest rate it offered was so attractive that four million users invested more than 10 billion renminbi in one month. With a well-functioning saving and lending platform, Ant Financial has become a complementary market intermediary directing capital to where it is needed. Finally, as Ant Financial functions online, the virtual credit market is independent from any physical branches of financial institutions, helping merchants in remote rural areas to find appropriate trade finance. This was unthinkable earlier in areas without physical bank branches.

As Ant Financial is a tangible institution with virtual banking licences, so it is or will be subject to regulations and supervision. This represents a key difference between fintech companies and other informal financing without “contractual obligations enforced through a codified legal system.” From a regulator’s perspective, fintech credit thus constitutes a form of alternative financing with more clarity and stability.

Fintech Reduces Transaction Costs for e-Payment

Thanks to e-payment and transfer services, consumers see fintech-supplied financial services as a way to reduce transaction costs. Transferring earnings home in a safe, quick and cost-efficient way, for example, is a fundamental concern for individuals working abroad. IMF statistics show remittances are very large, especially in low-income countries, and often are costly – notably for smaller remittances, such as those under $200.

By allowing quicker and less expensive transfers, fintech companies have provided concrete windfalls for those with the greatest need and are helping us move towards achieving the United Nations’ Sustainable Development Goals. Alipay in China is just one example. Other developing countries have pioneers, too. Vodafone launched M-PESA in Kenya in 2007. Kenyans use M-PESA for salary payment and wage transfer. Studies show that digitizing transfer payments significantly reduced travel and wait times, thereby raising the income of the rural Kenyan households using M-PESA by 5%-30%.

Indonesia has adopted a similar strategy to promote financial inclusion, with the development of Digital Financial Services (DFS), or Layanan Keuangan Digital in Indonesian. DFS allow e-money issuers to provide basic bank account and other financial services via branchless banking agents, like M-Pesa kiosks. The IMF finds DFS “a promising channel to overcome geographical barriers to financial inclusion.” Another example is the platform Alipay Hong Kong has developed with GCash, a mobile wallet created by the major telecommunication provider in the Philippines. GCash will now enable online remittance transfers between Hong Kong and the Philippines, helping 200,000 Filipinos living in Hong Kong, who remit an estimated $700 million a year.

The rapid expansion of financial digitization significantly lowered the costs of access to finance, especially for the lower-income cohort of the population. In this area, fintech is really “banking” the previously unbanked. Although they may have no bank account, they can still benefit from financial products as long as they have a mobile phone. It gives access to micro-loans and helps social mobility. Reduced transaction costs have also made access to other financial services, such as investment and financial risk management options, more affordable, making households more resilient to financial shocks and improving the country’s overall financial literacy.

Looking into the Future – Challenges Facing Fintech

Fintech has certainly set in motion innovation in the traditional financial sector. The examples from Asia and Africa show that mobile-based services are providing financial services that traditional banks cannot, because of a lack of credible data or geographical obstacles. By banking the unbanked, fintech is likely to prompt traditional players in the sector, like banks, to innovate. This would in turn accelerate the sector’s regime change.

To harvest the fruits of technical innovation while mitigating new risks, fintech must also strategize on how to deal with emerging challenges, of which we see three.

“Even when the sun is still shining, it is advisable to run stress tests on fintech firms’ resilience to potential shocks.”

Credit default risk. So far, this risk has been low, but it could become more serious. Emerging market economies performed very well through 2017. Given that the ability of SMEs to pay their debt is strongly correlated with economic cycles, no major default risks were foreseen or took place. However, proper safeguards need to be established to prevent major credit events in the future. Enhancing micro-prudential measures within fintech firms is one approach. Ant Financial likely imposes a floor credit score to Alibaba vendors assessed against a number of quantitative criteria; this constitutes an internal creditworthiness check tool. Ant Financial’s loans have short maturities and loan renewal is likely to be dependent on a firm’s past default history, another built-in safeguard. However, when the credit extended by fintech firms grows too big, emergency plans must be conceived. Even when the sun is still shining, it is advisable to run stress tests on fintech firms’ resilience to potential shocks. On the other hand, central banks need to think whether to include fintech companies within the perimeter of central bank emergency liquidity assistance or public guarantee schemes. Of course, this type of public assistance or guarantee will depend on the licences that fintech firms have been granted in different jurisdictions.

“Financial services created through technical innovation have often opened up new business areas that lack official oversight.”

Financial supervision and regulation. Financial services created through technical innovation have often opened up new business areas that lack official oversight. Understandably, it takes some time for regulators to adapt to emerging technological innovations, and to get used to the complexity of financial digitization. For instance, the breadth of fintech activities may require various licenses, thus the supervision from several regulatory competences. How to offer a holistic and coherent approach to the oversight of fintech activities remains a key policy issue. In general, one should expect a dynamic relationship between fintech firms and financial regulators. Financial technology encourages regulators to adopt new tools and thinking while new regulations will likely affect the field in which fintech firms play in the future. In Indonesia, the Bank of Indonesia has established a fintech office and the Indonesian Financial Service Authority has set up an internal cross-departmental group to promote sustainable growth of fintech services and mitigate risks to the financial system. Hong Kong adopted a “sandbox” strategy to test new financial innovations within a well-designed supervision framework. In this context, the IMF’s Lagarde called in a speech for coordinated global action to promote best practice and to avoid a regulatory “race to the bottom” given the varying regulatory stringency towards financial innovation in different countries. This is especially important when we think about the need to mitigate fraud risks and misuse of financial technology for crime and terrorist financing due to its swiftness and anonymity (e.g., distributed ledger technology and asset encryption).

Data protection. With market developments and the increased awareness of users’ rights, internet users are paying ever-greater attention to confidentiality of personal data and protection of their rights. How to benefit fully from financial innovation while preventing misuse of personal information will be a major topic not only for consumers but also for innovators. Respecting personal information also forms the basis of trust and confidence in any future financial services. In this regard, Europe has taken a step forward with the introduction of the EU General Data Protection Regulation (GDPR), which emphasizes client consent and the right to data erasure, while promising severe consequences for breaches. Although the most developed and valuable fintech firms are based outside the EU, there might be regulation spill overs that would be a key issue to address for fintechs willing to enter the European market.

Is Fintech the Future?

In China, Kenya, and Indonesia, fintech companies are already easing credit market frictions and reducing transaction costs – two distinct aspects of financial inclusion that policymakers are trying to promote. Fintech companies often start as online shopping and telecommunications companies, then quickly move to building up a network of customers and providing them with financial services. This process is described by the Bank of International Settlements as the “DNA” of fintech firms, namely the interaction between “data analytics, network externalities and interwoven activities.” One key contributing factor is fintech’s ability to secure and retain a large number of regular users, thus building big data on users’ behaviours and nurturing trust. After all, as many policymakers and key fintech players acknowledged in a policy panel during the IMF/World Bank Spring Meetings in April 2019, trust, not technology, is the big challenge that fintech needs to address to achieve their full potential and generate economic and social benefits.

In line with a number of other reports that were published on fintech and financial inclusion recently, we believe it is the right time to emphasize the policy relevance of the topic for the coming years. This is especially true because the first three-year Financial Inclusion Action Plan agreed in 2017 by the G20 countries ends this year. Policymakers will need to take stock of what has been achieved within the G20 Working Group on Global Partnership for Financial Inclusion and envisage even bigger steps towards this common global objective. It is thus essential for researchers and technical experts to shed light on the considerable social impact and promise fintech is offering and to find solutions to contain potential risks.

Fintech, and with it our more digital world, are changing our lives every day. Some things we know or have known might become obsolete in the future. Kalin was recently looking for a “piggy bank” for a family member’s baptism. His dream was that the baby would keep it for the rest of her life. It made him wonder – when she is older – will she even be using these small pieces of metal called coins?

Photo credit: Zijian Zhang