The term “family office” couldn’t be a more innocuous moniker. These entities, shrouded in secrecy, are close, trusted friends and confidants to wealthy families and ultra-high-net-worth individuals, providing them with advice on how to invest the family money. Their influence extends across those “substantial families,” their family businesses and family foundations, to succession planning and safeguarding the family’s legacy, prosperity, and harmony.

The newly released seventh biannual survey by the Wharton Global Family Alliance (WGFA) brings rare insights into how family offices function. “A key learning is that family offices are a lot more than simply private asset management companies,” said Wharton management professor Raphael (Raffi) Amit, cofounder and chairman of the WGFA. “They are in fact the backbone for a family, addressing a broad range of issues beyond investment management that contribute to family harmony and prosperity.”

The WGFA combines “the practical expertise of highly successful global families and rigorous scholarly analysis from Wharton researchers,” according to an executive summary of the WGFA survey.

Financial Performance in Investing

The WFGA survey tracked the investment avenues of family offices across 21 countries in Q1 2024, the size of the assets they manage, and the returns on those investments. More than 40% of the respondents had assets under management of more than $1 billion, while a quarter of them had assets of between $500 million and $1 billion; the remainder had less than $500 million.

About 45% of those respondents earned average annual net returns of more than 10% over the five-year period ending December 2023; none of them reported negative net returns in that period. The top three asset classes were public equity (34%), private equity (22%), and real estate (10%).

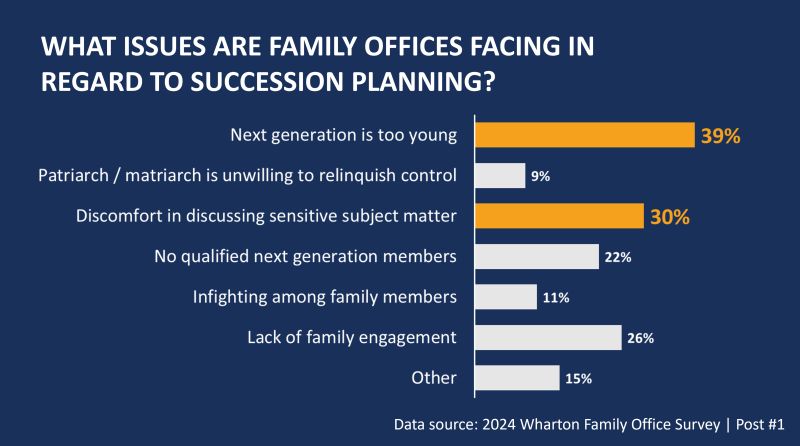

Even as the average family office appears to have made sound investments in its future wealth, they face disconcerting trends on other fronts. For one, the role of the next generation in the family office is fairly limited: about a fifth of next-generation members are not involved in the family office, and only about 12% of them may work in the family office in the future.

According to Amit, the upshot of those findings is that the next generation in substantial families may not be ready to deal with the complexities of succession in ownership, management, and control.

“Succession planning isn’t just a good business process; it’s a safeguard for a family’s legacy, harmony, and sustained success,” Amit said. “Without it, the risks extend beyond the family, often impacting professional teams as well, as new generations seek to establish their own leadership and step away from ‘dad’s team.'”

Hurdles to Succession Planning

A key finding of the survey is that only a third of family offices have formal or informal plans for ownership, management, and control transitions; only a third of stakeholders are aware of these plans. “Clearly, families struggle with putting structure, process, and formality around family succession and transitions,” Amit said in one of a series of LinkedIn posts published late last year jointly with Paul Carbone, cofounder and vice chairman of Pritzker Private Capital. “That’s because they face overarching challenges during transitions from concentrated to dispersed ownership.”

Those challenges include reaching consensus on major issues; balancing diverse interests/viewpoints of family members; managing the liquidity needs of different generations while trying to preserve the real value of the family’s wealth; and attracting and retaining outside talent while keeping family members involved in the business. “Neglecting to deal with those challenges can have serious implications for family cohesion, legacy, and the family dynamic,” Amit said.

Those disconnects may have something to do with the mission statements of family offices. As it happens, only half of family offices that were surveyed have a mission statement. “Failing to have a mission statement that has been developed by the family, and which has gained broad family acceptance, will only make a period of transition all the more dangerous,” Amit cautioned. “Perhaps that is why more families are now turning to non-family members to lead, and merit-based factors — like expertise in family dynamics and industry experience — are prioritized over seniority or ownership when selecting the next leader.”

Slow to Adopt AI, New Technology

Another potentially worrisome trend is the slow pace of adoption of AI and other emerging technologies by family offices. “The implications of these results are significant as the cost profile of family office investing may remain higher and their investing effectiveness negatively impacted, potentially resulting in suboptimal returns that could erode over time,” Carbone said in a LinkedIn post. “Consequently, families may need to consider outsourcing more of their investment strategies to those with a competitive cost structure and technological advantage.”

Family offices may be slow to embrace AI and other technologies because they want to avoid the pains on the learning curve and avoid false starts, Carbone wrote. “Broader adoption will first require existing challenges to be overcome and trust to be built in these powerful tools.”

“Failing to have a mission statement that has been developed by the family, and which has gained broad family acceptance, will only make a period of transition all the more dangerous.”— Raphael (Raffi) Amit

The survey pointed to other technology aspects that may warrant attention: On average, family offices employ less than one IT professional, and few of those are cybersecurity experts. Also, only half of respondents have an IT disaster recovery plan.

Direct Private Investments: Surprising Trends

The survey revealed that nearly half of the families it tracked made direct private investments, without staffing up with private equity professionals. Surprisingly, only 12% of families consider investing in other family businesses central to their strategy. That is “despite the clear advantages family capital holds when invested alongside like-minded users of capital who understand its unique value,” Amit noted.

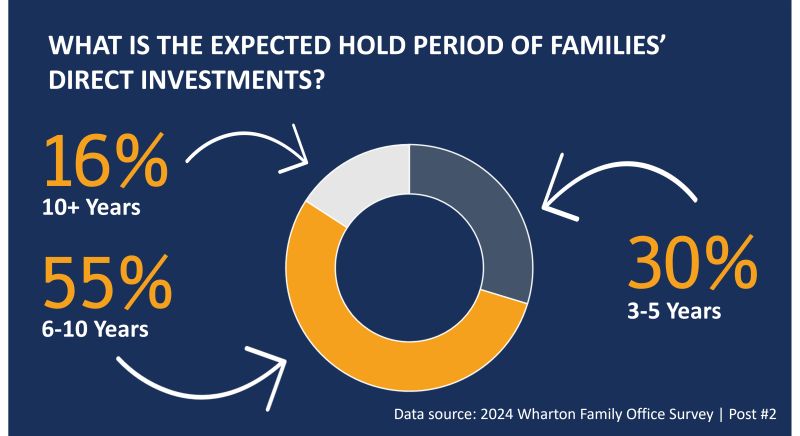

A puzzling trend here was that only 15% of families hold investments for more than 10 years. Specifically, the survey showed that family offices held 30% of investments for 3-5 years, while 55% of investments were held for 6-10 years.

Seventy percent of those direct private investments are syndicated, “with families prioritizing trusted relationships, value alignment, and the ability to add value when selecting syndication partners,” Amit said.

Another remarkable finding is that 60% of families make cross-border investments, which reveals their comfort in “navigating the risk of going outside their borders, particularly when they often lack in-house expertise and only hold a minority position.” The reliance on syndicates may explain that confidence, as many families partner with those who have the necessary knowledge in unfamiliar geographies, Amit pointed out.

ESG, Philanthropy, and Human Capital

The survey also covered how family offices go about their ESG investing, philanthropic activities, and human capital. About 35% of respondents have made or plan to make ESG investments. Their approaches are thematic investing such as clean energy, gender equality, health care, and water (33%); integration of ESG factors into analysis (25%); and negative/exclusion-based screening, such as avoiding investments related to tobacco, alcohol, or weapons (18%).

About 65% of philanthropic activities are through family foundations. Other philanthropic avenues were giving to charities (31%), giving directly to specific causes (25%), and donor-advised funds (22%). ESG activities and impact investing attracted only 8% of the share of philanthropy.

Family offices invested in their human capital by funding continuous education programs. Those efforts have paid off, it appears: The “vast majority of investment and accounting professionals remain with the Family Office for five years or longer,” according to the WGFA executive summary.

Read more about the report and download and executive summary here.