Casper, a direct-to-consumer mattress start-up headquartered in New York City, successfully completed its initial public offering in the first week of February. Its experience shows the good times may not last for other so-called “unicorns,” writes David Erickson in this opinion piece. He is a senior fellow in finance at Wharton and co-teaches a course on Strategic Equity Finance. Before teaching at Wharton, Erickson worked on Wall Street for more than 20 years, helping private and public companies raise equity strategically.

With Casper’s IPO pricing well below its initial range in early February, the market is still skeptical of “unicorns” that were awarded $1 billion-plus valuations in the private equity market. Less than a year ago, the company had raised capital in the private market at an approximate $1.1 billion valuation. With its IPO pricing at $12 per share (down from the original $17 to $19 price at which it was marketed), Casper’s public equity valuation is some $490 million — less than half the value of its last private round.

Normally, when an IPO prices significantly below the range that it markets its IPO, it is usually because of “market conditions.” While concerns about the coronavirus have been weighing on the equity market over the last few weeks, during the week of Casper’s IPO pricing, the equity market had rebounded significantly with NASDAQ reaching a record high on the day of pricing.

As a matter of fact, with the very strong performance of last year’s U.S. equity market, you would also have expected a strong performing IPO market in 2019, with many of the largest and high profiled IPOs leading the way. While some of the 2019 unicorn IPOs like Zoom and Beyond Meat have done well, the most high-profile names — such as Uber and Lyft — have struggled below their IPO prices for most of the time since going public. The spectacular debacle of WeWork, which never made it to market after its initial filing in August, stunned the market. WeWork went from a unicorn valued by SoftBank’s January investment at $47 billion to a restructuring story valued at approximately $8 billion of equity (even though pro-forma for the deal, SoftBank, with more investment, would bring its total equity investment in WeWork to approximately $13 billion).

Haunting Signals

What messages does the Casper IPO send the unicorn market? For those companies (and their founders and backers) that are considering going to the IPO market, a few things should be considered:

- Valuations in the private market are interesting, but they may not be the reference point for going public. With Casper pricing its IPO at less than half of its last private round, it is clear that public equity investors are going to be more skeptical of the valuations achieved in the private markets for many of these unicorns. Also, to accept such a significant discount to do the IPO, one reason could have been that Casper may have had limited interest for additional funding in the private markets at its recent valuation levels (though existing investors, NEA and IVP indicated interest in buying up to $20 million in the IPO).

- Companies trying to position themselves as “tech companies” to get a higher valuation multiple probably actually need to be “tech companies.” As you read Casper’s amended S-1, it seemed in various sections to position itself as a “sleep technology” company and “a pioneer in the sleep economy.” Specifically, Casper opened the Prospectus Summary section by describing itself thus:

As a pioneer of the Sleep Economy, we bring the benefits of cutting-edge technology, data, and insights directly to consumers. We focus on building direct relationships with consumers, providing a human experience, and making shopping for sleep joyful.

This for a company that in its Risk Factors section outlined that “a significant portion of our revenues is derived from our mattress products….”

For investors, this may have reminded them of reading the We Company’s S-1 in August 2019, where We opened the Prospectus Summary section with “Our Story” by describing the company as:

Our mission is to elevate the world’s consciousness. We have built a worldwide platform that supports growth, shared experiences and true success. We provide our members with flexible access to beautiful spaces, a culture of inclusivity and the energy of an inspired community, all connected by our extensive technology infrastructure. We believe our company has the power to elevate how people work, live and grow.

- A path to profitability does matter. While companies can still go public losing money, there again will be more scrutiny for companies that have raised a significant amount of money and used those funds to grow its top line, while losing a significant amount to generate this revenue. For investors, this is probably even more important for a “direct to consumer” company that operates in a highly competitive market, where its primary product (i.e., mattresses) have a long replacement cycle.

Implications for the Unicorn Market

Some four years ago, I wrote a Knowledge at Wharton article entitled “Why We Should Expect Some Thinning of the ‘Unicorn’ Herd,” where I suggested that the 144 unicorns at the time (as measured by CB Insights) would likely see a thinning – some would go public; some would sell; some would need to find alternative paths (i.e., revise their model, etc.); and others would hit the wall. While some of that did happen, the number of unicorns is now more than three times it was at that time. (CB Insights’ current number of unicorns is 447.)

I missed two primary things back then:

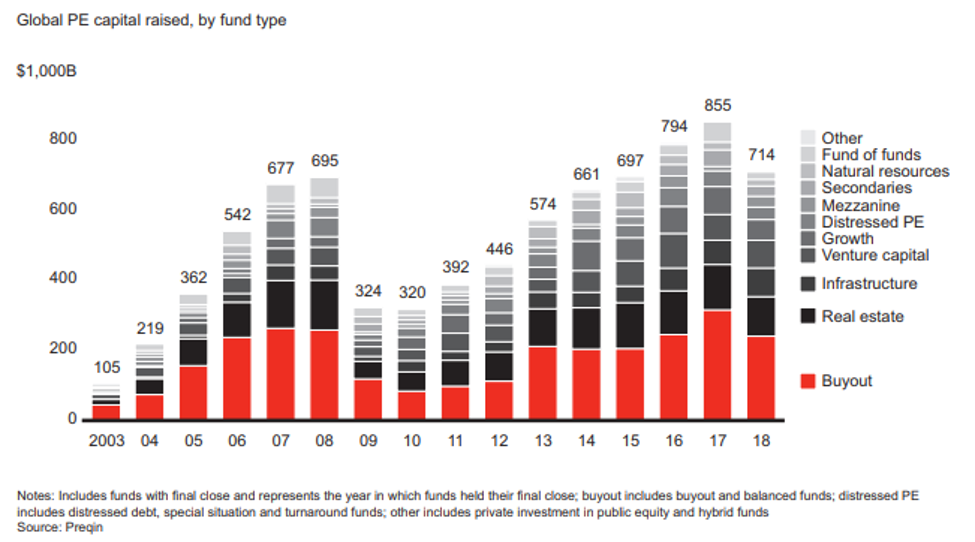

- The continued (and growing) liquidity of the private equity market. In the years following 2000, with the correction from the “tech bubble,” there was a considerable decline of venture capital and growth equity investing. Today, there are more investors participating in the private market including mutual funds, hedge funds and more private equity firms. They are raising a ton of new money. As seen in the graphic below from Bain’s Global Private Equity Report 2019, more than $3.7 trillion of new money was raised in the five years through 2018. While not all of that has gone to the unicorn market, a significant portion has, as fewer buyouts have taken place in recent years.

2. A significant strategic M&A “bid” in recent years. With the strong performance of the U.S. equity market in the last few years, many companies became more acquisitive with their rising stock prices. This strategic M&A interest has also included acquiring interesting unicorns – from Cisco Systems buying AppDynamics in the midst of its IPO roadshow to Visa acquiring Plaid a few weeks ago. This strategic “bid” has supported strong valuations for many unicorns, and encouraged further investment in “hot” areas such as AI and fintech technologies.

While these two factors have been powerful drivers for the continued growth of the unicorn market, now with 447 unicorns and a less robust IPO market for many of these companies, I don’t believe most of these companies will be around in, say, the next five years.

As a result, I believe that for many of these unicorns (those that are losing money and have some distance to go to cash flow break-even) the alternatives available will be similar to the ones I articulated in 2016.

Specifically, some unicorns will:

- Go public with no/minimal adjustment (like Zoom)

- Go public with a major valuation adjustment (like Casper)

- Raise money privately (if there is still appetite)

- Sell the company (like Plaid)

- Revise the model to get to break-even faster (like We, which will likely slow growth and potentially lessen interest and excitement in the company)

- Hit the wall (or as Marc Andreesen, founder of leading venture firm Andreesen Horowitz, stated in a 2014 tweet: “When the market turns, and it will turn, we will find out who has been swimming without trunks on: many high burn rate co’s will VAPORIZE.”)

That is why Casper’s IPO may spook the unicorn market. However, for the company, Casper now has significant public capital to continue to grow its business; diversify its potential funding sources going forward; and offer a public “currency,” which may make it easier for them to make acquisitions (if they desire).