The Great Recession, as harrowing as it was a decade ago, seems to have faded from public memory. It is safe to say that a general sense of normalcy pervades the lives of most Americans. Today, the economic environment could not be more optimistic: The U.S. stock market is hitting new highs, unemployment is at historically low levels and home prices have rebounded to their pre-crisis highs. Banking profits have roared back.

Has the global financial system truly recovered? “We have seen numerous regulatory reforms since the financial crisis, and many of them have undoubtedly enhanced the resilience of the financial system,” says Wharton finance professor Richard Herring, who is co-chair of the Shadow Financial Regulatory Committee. “Most of the reforms have aimed at reducing the vulnerability of banks to another crisis. Equally important, however, are the reforms aimed at enabling the authorities to deal with a bank insolvency without imperiling the financial system.”

According to Herring, crisis prevention efforts have focused largely on requiring banks to hold more and higher quality capital, as well as increased asset risk weights and capital surcharges for systemically important global financial institutions. They also include the introduction of a total loss-absorbing capital and global leverage ratio, liquidity requirements as well as heightened prudential supervision including the implementation of stress tests. “These measures have unquestionably enhanced the capital strength of most banks and reduced their vulnerability to a liquidity crisis.”

While Herring and other observers have raised questions about the design and cost-effectiveness of many of these measures, he believes overall that “they have strengthened the safety and soundness of the banking system.” He notes that it is also critical that there be an orderly process in place to enable even the largest banks to fail safely. “These reforms are less well known, but equally important. They include living wills and resolution policies designed to accommodate the insolvency of even a very large bank without causing damaging spillovers to the rest of the financial system or costs on taxpayers.”

“Most of the reforms have aimed at reducing the vulnerability of banks…. Equally important, however, are the reforms aimed at enabling the authorities to deal with a bank insolvency without imperiling the financial system.” –Richard Herring

Wharton finance professor Krista Schwarz agrees that the banking industry is “much safer than it was pre-crisis,” thanks to the financial reforms of the Dodd-Frank Wall Street Reform and Consumer Protection Act in the U.S. and Basel III, which is a set of voluntary international banking regulations requiring minimum capital requirements and leverage ratios, as well as enhanced risk capture, adequate liquidity, among other stipulations. “Leverage is down, reducing exposure, and banks have much larger liquidity cushions to protect against potential shocks,” she adds.

U.S. vs. Europe

European banks, however, have not fared as well as American banks. “U.S. banks have recovered much more rapidly and completely than their European counterparts. Primarily this is because the U.S. regulators understood that many of the large U.S. banks were subject to doubts about their solvency,” Herring says. To deal with this problem, he explains, “the U.S. authorities instituted a Supervisory Capital Assessment Program early in 2009 in which the 19 largest banks were required to estimate their capital adequacy under an adverse macro-economic shock and, if they failed to meet capital adequacy requirements, they were forced to obtain enough financing from the Troubled Asset Relief Program (TARP) to obtain enough capital to meet all safety and soundness requirements even under an adverse economic scenario.”

Critically, Herring notes, “the authorities took the bold, but important, step of making the results public. This was a bold measure because in fact 11 of the 19 banks failed the stress test. This transparency greatly increased public confidence in the process and the results — and fundamentally restored confidence in the U.S. banking system.” In contrast, “the Europeans were much slower to recognize that many of their banks were fundamentally insolvent and when they finally implemented stress tests, the [results were] so weak that the Irish banks passed only weeks before the entire banking system collapsed.”

Herring adds that “the fundamental problem [the Europeans] faced is that they lacked the important back-up of a facility comparable to TARP. They lacked financial resources to recapitalize banks that were inadequately capitalized, which led them to cover up rather than address the problem. Although most European banks have managed to recover, the process has been slow and has impeded economic recovery. Banks have been impaired in their ability to perform their fundamental role in financing investment.”

Schwarz notes that European banks are far behind the U.S. in tightening regulations. “Europe never undertook an equivalent of TARP, and European regulators have not subjected their banks to stress tests as credible and rigorous as those of the Fed. An illustration of this can be seen right now in the exposure of European banks to the Turkish devaluation, a shock that they should have been easily able to absorb.”

“Leverage is down, reducing exposure, and banks have much larger liquidity cushions to protect against potential shocks.” –Krista Schwarz

Wharton finance professor Itay Goldstein concurs that the U.S. “did a better job stabilizing the financial system more quickly and more thoroughly than Europe. You can see that banks in Europe continued to have problems for a longer period, and the overall economic problems in Europe [stayed] longer and [were] deeper than in the U.S. I think to some extent this is still the case today. By and large the banking system here is in better shape than in Europe. Europe has some issues that are specific to them that they still have to deal with. Most of it is about coordination across the different countries in the EU.” One complexity: There are local central banks in European countries, and they have to coordinate their actions with the European Central Bank (ECB), he says.

Another complicating factor is Britain’s exit from the EU. “Britain was an important part of the banking regulation in Europe, and now … they are leaving the EU. No one knows exactly how this is going to end, and it clearly puts some uncertainty around [the situation],” Goldstein says. Plus, “you see other issues coming up — political movements in different countries that call for separation, and some of them are becoming more prominent. All of these issues are just increasing the uncertainty about the stability of the banking union and central regulation … [and] are clearly weighing on the European banking system.”

Herring points to another challenge. “The closely related problem is that the European Union is trying to run a monetary and banking union without a European fiscal policy,” he says. “Because European banking regulations do not address differences in country risk among European member states, European banks are often heavily exposed to member countries that encounter debt problems. Thus, in addition to the financial crisis, Europe has had to contend with a series of country debt crises.” At the time, Portugal, Italy, Ireland, Greece and Spain could not repay or refinance their government debts or bail out their own distressed banks without help from the ECB, International Monetary Fund (IMF) and more stable EU nations.

Global Efforts

Getting the financial crisis under control globally took a coordination of policies by the G20 governments, wrote IMF Managing Director Christine Lagarde in a recent blog. “Countries with banking problems limited the drag of flailing financial sectors on the real economy — through measures such as capital support, debt guarantees, and asset purchases. Central banks slashed policy rates and later sailed deep into unknown seas with unconventional monetary policy. Governments propped up demand with large fiscal stimuluses.” IMF did its part too, she said, putting $250 billion into the system.

But more needs to be done. “Too many banks, especially in Europe, remain weak. Bank capital should probably go up further. ‘Too-big-to-fail’ remains a problem as banks grow in size and complexity,” Lagarde wrote. “There has still not been enough progress on how to resolve failing banks, especially across borders. A lot of the murkier activities are moving toward the shadow banking sector. On top of this, continued financial innovation — including from high frequency trading and fintech — adds to financial stability challenges. In addition, and perhaps most worryingly of all, policymakers are facing substantial pressure from industry to roll back post-crisis regulations.”

“Britain was an important part of banking regulation in Europe, and now … they are leaving the EU. No one knows exactly how this is going to end, and it clearly puts some uncertainty around [the situation].” –Itay Goldstein

The financial crisis has cast a long shadow. Lagarde said 24 countries “fell victim” to banking crises, and economic activity has not rebounded for most of them. Public debt in advanced economies increased by more than 30 percentage points of GDP, which she attributed to economic weakness, efforts to stimulate the economy and for bailing out failing banks. In the U.S., the economy in 2017 was 12 percentage points smaller than it would have been if the 2007-2009 Great Recession had not happened, based on its pre-crisis growth trend, according to the Federal Reserve Bank of San Francisco. Such a substantial loss is “unlikely” to be recouped, the central banker said, translating to a lifetime present value income loss of $70,000 for every American.

Indeed, the road back from the brink has been “long and slow,” said William Dudley, former president of the Federal Reserve Bank of New York, in a November 2017 speech in New York. Nine million jobs were lost in the crisis and eight million homes were foreclosed in the worst recession since the Great Depression. Bear Stearns was acquired in a fire sale by JPMorgan Chase, Lehman Brothers went bust and giant insurer AIG had to be bailed out to stem the spread of losses. The securities lending program of AIG’s non-insurance unit was the major source of its liquidity problems, according to a U.S. Government Accountability Office. (The impact on the rest of insurers was fairly limited.)

Dudley said it took eight years for job growth to rebound back to the Fed’s target level — but residual impacts remain. He pointed to the Federal Reserve’s balance sheet, which remains bloated after three rounds of quantitative easing, the presence of “significantly” higher public debt, and “substantial damage to public trust in the nation’s government and financial institutions.”

Banks Refocus and Restructure

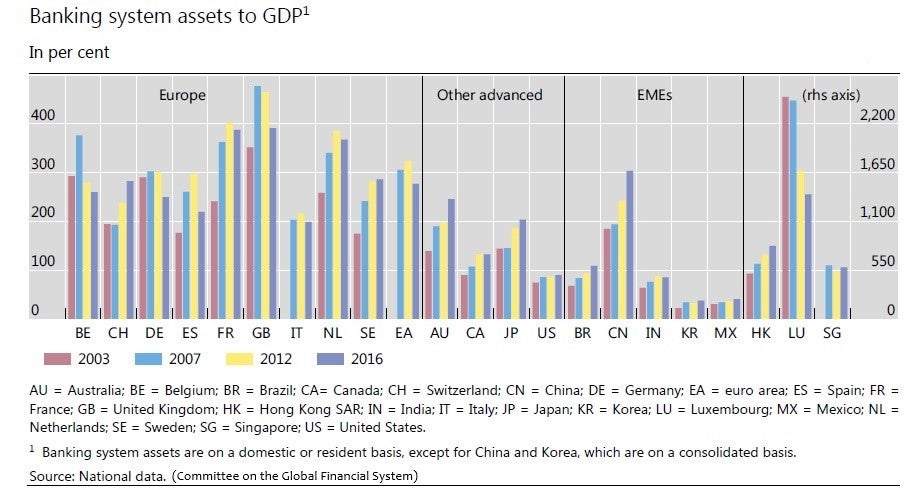

Today, U.S. and European banks affected by the crisis have changed. They have been reassessing and adjusting business strategies, growth plans, balance sheet positions, cost bases, organizational structures, scope of activities and geographic presence, according to a January 2018 report by the Committee on the Global Financial System (CFGS), a central bank forum that monitors global financial markets for stability and other issues.

In general, banks have moved away from holding “complex or capital-intensive assets” towards assets that typically pose less risk, the report said. Moreover, “many large banks have reduced their exposure to trading assets and more complex securities.” Another trend among big banks is that they have decreased activities in over-the-counter derivatives due to new regulations. This is particularly apparent in global, systemically important banks, according to the CFGS. In the meantime, their common equity capital ratios have risen “significantly” since the crisis.

“[The] European Union is trying to run a monetary and banking union without a European fiscal policy.” –Richard Herring

Banking systems that are members of the CFGS also saw annual average growth fall to 4% from 2008 and onwards, compared to about 12% from 2003 to 2007, right before the crisis. In Europe, the ratio of bank assets to GDP was a mixed bag, plunging in some and rising in others. Banks in emerging markets have not been as impacted by the crisis and continued to show robust growth, the report said. In particular, growth of the Chinese banking system jumped to around 310% of GDP from 230% between 2010 and 2016. It is now the largest in the world.

Two European banks that saw significant changes were the Royal Bank of Scotland (RBS) and Switzerland’s UBS. The report said that RBS failed in October 2008 and had to be rescued by the U.K. government. Since then, the bank has taken steps to strengthen its balance sheet. It decided to focus on lending to U.K. businesses and households while shrinking its investment banking activities. RBS also reduced its global operations down to 13 countries from 38. The bank is expected to continue in a period of major restructuring through 2019.

The Swiss government rescued UBS in 2008. Since then, the bank has moved away from investment banking activities and refocused on its other businesses, in particular global wealth management and retail and corporate banking in Switzerland. UBS also said its investment bank operations would exit a “substantial” number of fixed income business lines, in particular complex and capital-intensive credit and interest rate products, according to the CFGS report.

The Next Crisis?

As American and European banks regrouped after the crisis, financial institutions in emerging market economies continued to grow. Chinese banks, in particular, rose to the top of the banking hierarchy with their massive assets. But they also took on a lot of debt. Goldstein says there is “potential fragility” building up in China. “Credit is growing, banks are growing, and those are known to be leading indicators of future declines and future crises. [It’s] possible things are going to start there.” But since China is centrally controlled, the outcome could differ from what happened in the U.S. and Europe, he adds.

“[In China,] credit is growing, banks are growing, and those are known to be leading indicators of future declines and future crises.” –Itay Goldstein

Herring’s view is that while it’s “impossible to forecast the source of the next financial crisis, I think it is unlikely to be set off by problems at banks in emerging markets. U.S. banks are relatively much less heavily exposed to emerging market banks and other emerging market borrowers than they were in 1982 or 1996, so direct exposures are unlikely to be a problem.”

But Herring also acknowledges that “a collapse of banks in a major economy like China could jeopardize economic stability more broadly if it should lead to a depression in the domestic economy. Emerging markets are now a much larger proportion of world GDP than they were 20 years ago, and our economy and that of other industrial economies is much more dependent on their health, but this is more an issue of economic interdependence than financial stability.”

Another area to watch is financial innovation, which brings risks along with benefits. It is a “double-edged sword,” Schwarz says. “New products can increase the efficiencies of capital markets, but they can also present new risks.” That’s especially true because technology typically innovates too fast for regulations to catch up. But one silver lining is that technology brings about much improved financial data collection and transparency, which helps alert policy makers and investors about potential risks, she adds.

For instance, Schwarz says, the new Office of Financial Research has detailed data on the composition of money market mutual funds on its website. The U.S. Commodity Futures Trading Commission now provides volume data for some of the over-the-counter derivatives such as interest rate swaps and credit default swaps, she adds. The Federal Reserve now publishes data on repo and funding rates. Moreover, “data aggregation is facilitated by the post-crisis implementation of central clearing for large parts of these markets,” Schwarz says. “Central clearing itself also provides risk reduction through diversification.”

“There will be another crisis, some day.” –Krista Schwarz

But, there are still risks, mostly outside of the heavily regulated banking system. Schwarz believes that money market mutual fund reform is incomplete. Also, she says, the “skin in the game” rules for securitizations exempt most mortgages.

While post-crisis reforms have made the banking system safer, Herring adds, “to some extent, they have simply shifted risk to other institutions and markets that are less carefully monitored and largely unregulated with regard to safety and soundness.” Risk is like the air in a balloon. By squeezing one part of the balloon, the pressure goes to another part of it. “If that part of the balloon is weaker, it may cause the balloon to explode,” he says.

Meanwhile, the U.S. government’s attempt to enhance oversight of the non-bank financial system through the Financial Stability Oversight Council has “fallen short of the kind of surveillance we should have in place to anticipate emerging sources of risk,” Herring notes. And part of the Dodd-Frank reforms constrain the Fed and the FDIC from providing the same sort of support for the banking system that they offered during the crisis. “This, in combination with the continuance of very low interest rates and mounting government budget deficits and spiraling public debt, means that it would be much more difficult for the authorities to deal with a problem if the new crisis prevention and resolution measures should prove to be inadequate.”

Schwarz concludes: “There will be another crisis, some day.”