Since President Donald Trump took office in 2016, there has been decisive and measurable movement toward deregulation and the reduced enforcement of existing regulations in many sectors, including the mortgage-finance industry. This has left an uncomfortable gap for those who believe that this trend leaves borrowers — and the larger economy — vulnerable to the avarice of lenders However, new research from Brian Feinstein, Wharton professor of legal studies and business ethics, shows states can step in to fill the gap through a mechanism called judicial foreclosure, which offers some legal protections and oversight to borrowers facing foreclosure. His policy brief, “State Foreclosure Law: A Neglected Element of the Housing Debate,” was published recently by the Wharton Public Policy Initiative. The brief was based on his paper, “Judging Judicial Foreclosure,” which was published in the Journal of Empirical Legal Studies. Feinstein joined Knowledge at Wharton to discuss his research and what it means in the political context. (Listen to the podcast at the top of this page.)

An edited transcript of the conversation follows.

Knowledge at Wharton: You point out that there is a gap in regulation or a trend towards deregulation on the federal level. How did this happen?

Brian Feinstein: The deregulatory shift mirrored the change in administration. With the Trump administration coming in, federal regulators eased up on mortgage lenders. The Consumer Financial Protection Bureau — the federal agency that’s primarily responsible for enforcing consumer finance laws — cut their enforcement activities by around 80%. In terms of monetary collections, restitution and fines are down by about 98% of what they were during 2015 and 2016.

Some see that more hands-off approach as appropriate. Regulation restricts consumer choice, after all. Others are concerned that without a cop on the beat, lenders will return to the same practices that helped get us into the financial crisis a decade ago. For those who are in that second camp, who recognize that the federal government is unwilling to act and that there should be some greater regulation, I would urge those folks to look to the states to police mortgage markets.

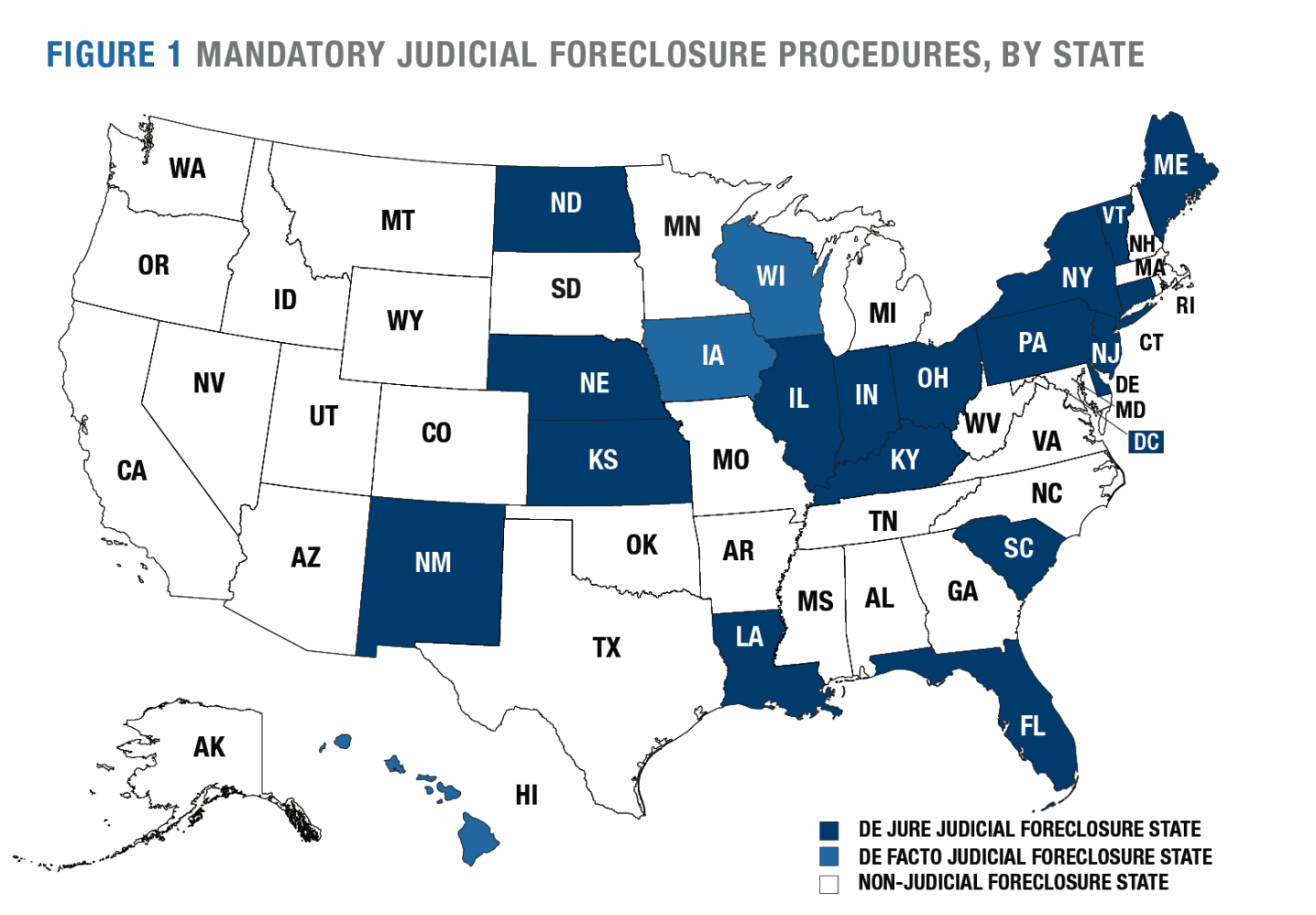

Knowledge at Wharton: Your brief advocates for state-mandated judicial foreclosure. How does that work, and how common is it right now?

Feinstein: It’s pretty common. Twenty-one states and Washington, D.C., right now require that lenders who want to foreclose on a mortgage file an action in state court to do so. What it means is that in those states, whenever there’s a foreclosure action — whenever a borrower has defaulted on his or her mortgage — you have a judge that examines both the lender’s adherence to the state’s foreclosure procedure and the lender’s behavior at the loan origination stage.

The judge can look at the loan and ask, “Did the lender adhere to the Truth in Lending Act? Did they make all of the required disclosures? Were there any deceptive practices? Given the borrower’s likely ability to pay, are the loan terms unconscionable?” Only when those questions are answered to the judge’s satisfaction would the judge sign off on the foreclosure.

“Lenders are less willing to originate new loans in judicial foreclosure states, so there are more potential borrowers who are rejected in those states.”

In the 29 other states, lenders can foreclose on the mortgage without going to court. In these states, it’s the borrower who has to affirmatively file suit to challenge the foreclosure. Of course, most borrowers in dire straits facing foreclosure don’t do that.

Knowledge at Wharton: In judicial foreclosure states, what are some of the benefits and potential consequences of that process? And what are the impacts on lenders and borrowers?

Feinstein: For borrowers, the primary benefit is that you get judicial supervision to make sure the lender meets all the requirements to foreclose. You also get a judge’s eyes on the mortgage. Is this mortgage appropriate for the borrower? Does it meet all the legal requirements?

The costs are contested. To the extent that judicial foreclosure slows down the foreclosure process, that’s going to raise the cost to lenders. Maybe lenders pass on these costs in the form of higher interest rates to borrowers, in which case the cost to the lender is taken on by the borrowers. Or maybe they adopt a more conservative lending posture, originating more prime loans, which are less likely to end up in foreclosure, and fewer high-risk subprime loans.

That’s what my research examines: How do the costs and benefits of this procedure play out? Do lenders change their behavior at the front end — their loan origination decisions — based on concerns that if the loan blows up, they’re going to have to face the cost, they’re going to have to face a judge in a judicial foreclosure state?

Knowledge at Wharton: How did you study this? I would think that real estate markets differ wildly from state to state, city to city, even neighborhood to neighborhood.

Feinstein: It’s tough because you can’t just compare these lender decisions in a state with judicial foreclosure with decisions in other states, or even within a given state, because there are so many other factors that could impact mortgage markets.

I compared loan application decisions in 14 pairs of neighboring states, where both states have substantially similar relevant laws, but for the fact that one state requires judicial foreclosure and the other doesn’t. Within these 14 pairs of neighboring states, I focused exclusively on areas near a state border, so metro areas that straddle a state border or other border regions. As you mentioned, even within a given state, mortgage markets and local economies can differ in different regions in the state, so this is a way to ensure that loans on both sides of the border are being made in an area with similar economic conditions and a similar mortgage market. Then I made sure that I was comparing loan applicants with similar demographic profiles, looking to buy homes in similar neighborhoods within those border regions. Finally, I focused on a subset of lenders that was subject only to uniform federal regulation at the time of the study.

Knowledge at Wharton: It would seem that the demographics of the borrower could really affect how they might navigate this judicial foreclosure process, because people who have a lot of resources and information at their disposal might be better able to navigate it than those who do not.

Feinstein: Yes, that’s exactly true. I controlled for those features and tried to pair similar borrowers in states on both sides of that border. The federal government has this Home Mortgage Disclosure Act dataset that examines every mortgage application, so tens of millions of mortgage applications a year. What’s the demographic profile of the borrower? Race, gender, income — all of these factors are identified in that dataset, so I could control for those. I paid special attention to race and ethnicity and gender, which are factors that many scholars have found really influence lenders’ decisions.

Knowledge at Wharton: Your research shows that judicial foreclosure alters lender behavior in some key ways. Could you explain what those are and how they might line up with the goals of those who feel like this industry needs to be regulated more?

Feinstein: There are really two ways in which judicial foreclosure impacts lenders’ behavior. First, lenders are less willing to originate new loans in judicial foreclosure states, so there are more potential borrowers who are rejected in those states. For the loans that lenders do originate, there are fewer high-risk subprime loans and more prime rates, which are less likely to end up in foreclosure in these judicial foreclosure states.

“Essentially, judicial foreclosure acts like a regulation.”

The bottom line here is that lenders adopt a more conservative lending posture in these judicial foreclosure states. Essentially, judicial foreclosure acts like a regulation. We can think of regulation as a legislature or a regulatory agency that issues an edict and then polices that regulated entities’ behavior at the front end. Well, judicial foreclosure is not like that. This is back-end behavior, after the loan has gone south in some way, but it has these front-end effects. It encourages lenders to modify their behavior at their decision whether or not to originate a loan, much like a regulation would.

Knowledge at Wharton: Judicial foreclosure does impose some costs on lenders and, in some ways, puts a lot of the onus on the lender. Do borrowers potentially feel the brunt of that?

Feinstein: Approved borrowers don’t. The folks that are being approved for loans tend to get better rates in judicial foreclosure states, and that’s important because another study found that around 40% of people who took out a subprime loan would have qualified for a prime rate — they just weren’t offered it.

To a large extent in judicial foreclosure states, these are folks that would have been offered a higher-risk subprime rate, but now because the lender is thinking, “OK, I’ll have to face judicial foreclosure if the borrower doesn’t perform,” the borrower is offered a prime rate, which is more likely to be performed on. The cost that’s faced, though, is those folks who want a loan but can’t get it. Recall that in these judicial foreclosure states, lenders tend to approve fewer loan applications. That means that there’s a group of people in these states that apply for loans that they would have received in a non-judicial foreclosure state, but here they’re turned away.

Knowledge at Wharton: What are some of the key takeaways for federal and state policymakers?

Feinstein: I think the main scholarly takeaway would be that judicial foreclosure looks a lot like a regulation. It’s something that lenders change their behavior ex ante, at the front end, based on this fear of being hauled into court at the back end. In terms of the takeaway for policymakers, I think state lawmakers who want to protect borrowers in their state and don’t think that Washington is up to the task ought to mandate judicial foreclosure and enact other foreclosure protections, because these sorts of back-end protections can alter lender behavior at the loan origination stage, just like a regulation would.

Knowledge at Wharton: What are some potential roadblocks to broader adoption of judicial foreclosure? Your brief includes a map that shows which states have it and which don’t, and they aren’t necessarily divided on political/ideological lines. For example, a lot of states in the Northeast that trend blue have it, but so does Kentucky, which trends red. Going forward, do you feel that political ideology could hinder broader adoption?

Feinstein: You’re right that currently there’s not any clear trend in which states have it and which don’t. Andra Ghent, a business school professor at the University of Wisconsin-Madison, has some research looking into the history of these laws. She found that many states, very early in statehood or even when they were colonies or territories, would either choose judicial foreclosure or non-judicial foreclosure and stick with that choice. In fact, in the past 80 years, only eight states have substantially changed their foreclosure procedure. She found that when a state originally made this decision, it was really for idiosyncratic reasons. For instance, in some states a particular judge just favored a particular procedure, and that became precedent. Eventually, the state legislature codified that precedent, and things continued on as they were.

I suppose the biggest roadblock here is just status-quo bias — that these laws don’t tend to change. In terms of other roadblocks, I probably ought to mention the banks don’t want it. Borrower protections are bad for their bottom line, and that’s why lenders have been successful at the federal level in rolling back some regulations and reducing enforcement.

A final roadblock is more philosophical — just the idea of government enacting measures that are designed to limit people’s financial choices. It’s preventing some people from getting subprime loans that they otherwise would have been approved for. That gives some people pause. There’s a deep strand of libertarian and utilitarian thought arguing against these sorts of measures. I take that critique seriously. My response is that when someone takes out a high-risk loan and then defaults on it, it doesn’t just affect them. There’s a study showing here in Philadelphia that when a residential property is abandoned, it reduces the land value of surrounding property by thousands of dollars. And as we learned in the Great Recession, sometimes these decisions in the aggregate can harm not only the borrower, but can harm in some instances the world economy writ large.

So, there are those significant roadblocks — status quo bias, the interest of banks, and this notion of limiting consumer choice — but I think policymakers interested in regulation ought to look at those roadblocks as being possible to overcome.

Knowledge at Wharton: Your map also shows some states that do not have judicial foreclosure were really hard hit in the Great Recession by the subprime crisis, like California, Nevada and Arizona. On the other hand, Florida has it and was also hard hit. Does that argue for or against broader adoption?

“When someone takes out a high-risk loan and then defaults on it, it doesn’t just affect them.”

Feinstein: It’s an interesting question. I’m hesitant to offer a thought either way because there are so many factors in these states. The reason I was so careful with this border design is because there’s so much else going on in, say, Florida or Nevada that can affect things like foreclosure rates. Had Florida not had judicial foreclosure, who knows how much worse their foreclosure crisis would have been.

Knowledge at Wharton: What’s next for this research?

Feinstein: With a co-author, Manisha Padi at the University of California, Berkeley’s Law School, we’re looking at the role that attorneys general play in policing mortgage finance. It has been 10 years since the Dodd-Frank Act was enacted. That law granted an unusual amount of power to state attorneys general to enforce both state and federal mortgage finance regulation. At the time that Dodd-Frank was enacted, the U.S. Chamber of Commerce and the American Bankers Association and other industry groups warned that empowering state attorneys general in this way would lead to inconsistent enforcement. So, you have 50 state attorneys general enforcing their own interpretation of federal law. When you have a switch between a Republican or a Democrat attorney general in a given state, you would see a wild swing in enforcement priorities. Therefore, they opposed that.

Manisha Padi and I take a step back looking at this. It has been 10 years since Dodd-Frank was enacted. Do we see that sort of inconsistency and these sorts of fluctuations? The answer is no. When a state attorney’s general office changes from Democratic to Republican control or vice-versa, we see mortgage markets displaying a remarkable degree of stability. So, we think that this critique of attorneys general enforcing state and federal mortgage finance regulation doesn’t hold a lot of water.