The United States could learn a great deal about infrastructure finance from Australia, which has paved the way for public-private partnerships in that domain, writes Wharton Dean Geoffrey Garrett in this opinion piece.

As an Australian, I’ve have been resisting the temptation these past few months to react to the Trump Administration’s big infrastructure plans with “The U.S. could learn a lot from my country.” The international comparison gambit rarely works well in America, and I don’t want to appear too parochial. But I have learned a lot from the Australian example, and I think now is the time to share, as the Trump Administration pursues a plan of federal infrastructure investment intended to stimulate state, local and private investments.

First, I interviewed the CEO of Australia’s Macquarie Group, Nicholas Moore, who’s been talking up his bank’s long track record of public-private partnerships (PPPs) in infrastructure at the recent Wharton Global Forum in Sydney .

Then I heard Gladys Berejiklian, the premier (essentially the governor) of Australia’s largest state, New South Wales, tell U.S. state governors in Washington, D.C., about her government’s big “asset recycling” program using privatization proceeds to pay for new public infrastructure.

Finally, I watched Glenn Youngkin, the co-CEO of The Carlyle Group, extoll the virtues of the Australian public-private infrastructure model (arguably inevitable for a big country with a small population) at a Wharton roundtable on infrastructure investment.

These events reinforced the three core truths about infrastructure:

- Building first-rate infrastructure — roads, bridges, ports, high-speed rail, airports, power grids, cell phone networks and fiber optic cables — is essential to realizing the full potential of all economies.

- The sheer scale of the global infrastructure challenge is so enormous that the only possible way to meet it is to find a much bigger role for the private sector.

- Savvy governments can ensure that increasing the role of the private sector in infrastructure furthers their mission of serving the broad needs of society.

It is a profound irony that America, arguably the world’s most developed and most market-friendly economy, not only has enormous infrastructure needs (The American Society of Civil Engineers 2017 report card gives the country a “D+”), but also continues with a government-led, if not government-only, mindset to taking on this challenge.

Airports are a striking example. Of the more than 500 commercial airports in the U.S., the only one that is privately owned and operated is in Puerto Rico. In contrast, while there are only 22 major commercial airports in Australia, 17 of them are now in private hands. In Britain, the home of privatization (thanks to Margaret Thatcher), only one in five airports remains in public hands.

The classical position on infrastructure is that it is a “public good” — something critical to society that “the market” would undersupply — and hence the natural domain of government. Importantly, this also implied that government pockets were deep enough that they could always pay for the infrastructure society needed.

Australian airports, not to mention British railways, belie both assumptions. The private sector clamored to get involved once government opened the door. Government opened the door because it realized the public purse was not fat enough to deliver the infrastructure the public wanted.

The U.S. doesn’t seem to be there yet, not even with the Trump administration’s infrastructure plans launched with great fanfare earlier this year.

Trump wants to spend $200 billion over the next 10 years. Despite the fact everyone agrees America’s infrastructure is in desperate need of repair and upgrading, getting this legislation through Congress is proving a hard slog — so much so that even the President admits any legislation must wait until after the midterm elections this November.

Why is this so hard, when everyone is irritated about potholes not fixed, let alone the decaying state of decades-old airports, freeways, ports and railways? Because public debt is high and rising, and people want tax cuts to make their lives better, not tax increases to build better infrastructure. Dramatically increasing government spending, even for essential infrastructure, is a very tall order.

What’s more, the ASCE estimates that the U.S.’s infrastructure needs are at least $2 trillion. The Trump plan would only be a drop in the bucket. The administration argues that incentives would create a large (7.5x) “multiplier” on every federal dollar by stimulating state, local and private investments to get closer to the needed total spend. But the Penn Wharton Budget Model says this multiplier is fanciful because most state and local governments are cash strapped and there are no clear pathways to engage the private sector on the investment side.

“Private sector involvement is widely seen as antithetical to the public good. Think about all the negative reactions to toll roads.”

The gap between infrastructure needs and governments’ ability to fund them is even bigger at the global level. McKinsey estimates that the world will have to spend $49 trillion on infrastructure by 2030 — more than $4 trillion every year for over a decade.

Governments in most emerging markets are hamstrung by chronic budget deficits, and the challenges to raising taxes are immense. They simply are not in a position to build the infrastructure their countries so desperately need.

Things don’t look much better when it comes to international organizations. The annual budget of the World Bank is only about $5 billion (0.1% of the global infrastructure need). China’s Belt and Road Initiative is much more ambitious, aiming to spend about $100 billion per year over the next decade in Asia, Africa and Europe. But BRI at this scale would only meet 2% of the world’s infrastructure needs.

There is simply no alternative other than to get the private sector to step up in a big way where infrastructure is concerned. Here Australia’s Macquarie Group is a world leader. It has been in the infrastructure game since 1994. It has over $100 billion in infrastructure assets under management –about 20% of the Group’s total AUM. This is obviously only a drop in the global bucket, but I wonder how many American financial institutions would jump at infrastructure financing were government to signal a change in its mindset.

Why hasn’t the U.S. embraced private sector involvement through PPPs the way Australia has? The simplest answer is more political than economic: Private sector involvement is widely seen as antithetical to the public good. Think about all the negative reactions to toll roads.

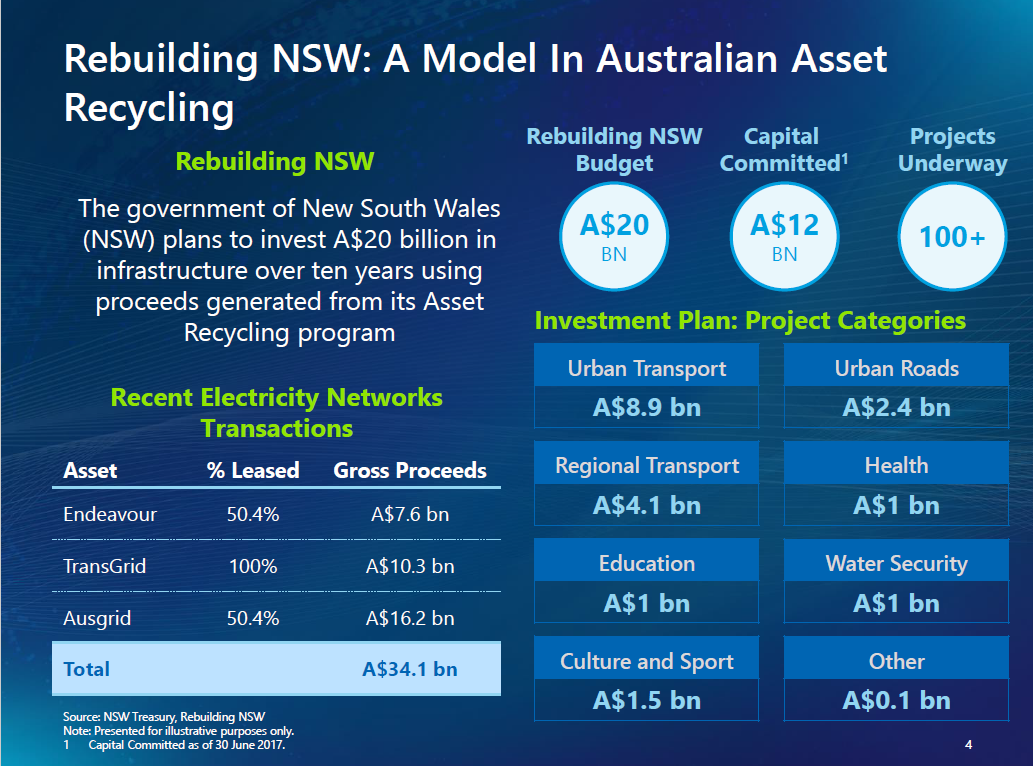

But this is where “asset recycling” comes in. The figure below, from Carlyle, shows what Australia’s largest state, New South Wales (NSW), has done. It has sometimes sold off — but more often “rented off,” i.e., sold-off operator rights for a finite period – state-owned assets, the biggest and best example being electricity. Then NSW has used the proceeds to build new roads and railways.

Note the implicit trade here: The NSW government decided to sell the rights to electricity distribution (the “asset” part), both because private sector operators were interested and because the government thought there was less (but certainly far from no!) “public interest” involved. But the “recycling” part is at least as important: The government pledged to spend most of the privatization proceeds on things NSW residents really want — notably better roads and railways.

What would such a program look like in the U.S.?

The sums in NSW, the home of Sydney, are about U.S. $26 billion in electricity network privatization revenues, with the bulk of the proceeds spent on new politically popular public infrastructure projects, and the remainder applied to reducing the government’s deficits and debt. NSW is about one-third of the Australian economy, and the Australian economy is about 7% the size of the U.S.

“Rather than banging on government for not delivering, maybe it is time to change the model.”

Do the math, and if the U.S. did asset recycling at the NSW scale, that would generate about $1.1 trillion dollars in sold-off infrastructure, with all that money then available to be spent on new infrastructure—more than five times the amount of money the Trump administration hopes to spend. In the U.S., most electricity is already in private hands, so the privatization target would have to be different. Consider airports.

Then let’s go global. The U.S. is a little less than one-fifth of the global economy. Globalize NSW and you would get $5 trillion — about the amount McKinsey thinks the world needs to spend on infrastrcuture every year.

These private-sector-generated numbers are still much smaller than global infrastructure needs. But they are also much larger than what we can ever reasonably expect the world’s governments to devote to infrastructure. Rather than banging on government for not delivering, maybe it is time to change the model. Bringing the private sector centrally into the big infrastructure challenge seems both essential and inevitable. So long as private gain can be married with public benefit (and NSW seems to have done this well), why wouldn’t Washington, and the world, try it?

(This article originally appeared on LinkedIn.)