Tanzanite is one of the rarest gemstones on earth and one of the most undervalued relative to its rarity. Given its scarcity, it would be reasonable to assume that it would sell at a high premium. Yet, with the price per carat ranging between US$300 and US$600, it sells for far less than diamonds. Unlike diamonds, however, it has no industrial use. But that fact alone does not explain Tanzanite’s low value. This article analyzes the structural reasons that have kept tanzanite from achieving its true potential, beginning with an historical and contextual overview of this remarkable gemstone. It then explores the economics of the tanzanite market and discusses the stone’s considerable potential to contribute to the development of Tanzania’s economy.

‘Gemstone of a Generation’: What is Tanzanite?

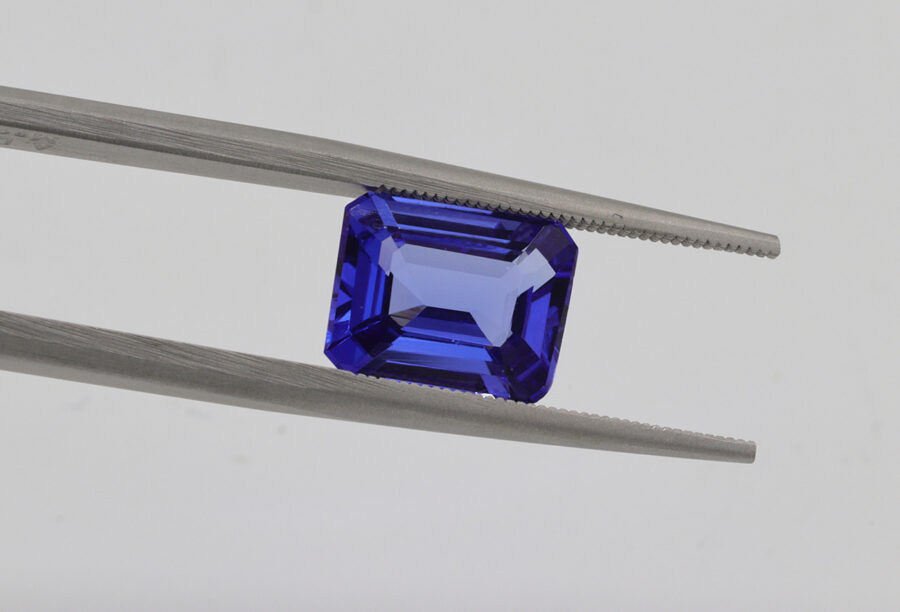

Tanzanite stone is a trichoic stone that reflects different colors, ranging from light blues or lilacs to deep indigos and violets. It was discovered in the 1960s and named after Tanzania by Tiffany & Co. The famous jewelry firm declared it to be the most beautiful stone discovered in the last 2,000 years. Tanzanite is so rare because it is found and mined in a small area only four kilometers wide and two kilometers long at the foot of Mount Kilimanjaro in the Manyara Region of Northern Tanzania. According to a Tanzanian geologist, the circumstances that led to its formation 585 million years ago were so exceptional that the likelihood of finding tanzanite anywhere else on earth is one in a million, making it a thousand times rarer than diamonds. At the current rate of mining, the geologist also estimates that the available supply will be depleted within the next 25 years. As a result, tanzanite is known as the “gemstone of a generation” because this generation will be the last one able to buy stones from the primary market before the supply is exhausted.

Tanzanite has enormous potential for Tanzania, but time is running out and the industry is in dire need of major changes and structural reforms. Currently, the worldwide wholesale market for rough tanzanite is estimated at US$50 million. To put that in perspective, a 2010 industry report by Bain & Company estimated the worldwide wholesale market for rough diamonds to be about US$12 billion. As Tanzania’s GDP is about US$28 billion, an increase in the market price or volume of tanzanite could have a significant impact on the local economy. But the window of opportunity is closing quickly as the likelihood of recouping near-term investments and benefiting from this rare resource is limited by the lifespan of the mines. While the Tanzanian government’s active involvement is necessary for the successful implementation of industry-wide reforms, its track record is less than flattering.

The government first became involved in 1971 when it nationalized all the tanzanite mines. Three decades of nearly nonexistent mining activity followed. Although the government wielded legal control, it lacked the knowledge and adequate human resources to operate the mines competently. Eventually, it returned ownership to private businesses. But in 2003, it intervened once again by imposing an export ban on rough stones larger than one carat. According to an industry veteran, the law served to foster a local cutting-and-polishing industry and to retain more added value within the country. However, it was poorly enforced, and the authorities failed to reduce smuggling. Thus, large quantities of gemstones in the rough continued to leave the country, to the detriment of larger and more established businesses. Furthermore, the country lacked the know-how and skills to develop the industry, at least until the emergence of TanzaniteOne.

According to its official website, TanzaniteOne is the largest and most scientifically advanced miner and vendor of tanzanite. It is wholly owned by Richland Resources Ltd., which is listed on the AIM sub-market of the London Stock Exchange as RLD. Despite its positioning, the company is small, with yearly revenues seldom exceeding US$24 million. It has been profitable only a handful of times since it was incorporated in 2004. While it is hard to understand why a large mining company of such a rare and beautiful stone has been unable to develop a lucrative market for itself, the answer can be found in a number of factors, including the Tanzanian government’s involvement in the development and exploitation of tanzanite, as well as the overall market structure.

Although the government wielded legal control, it lacked the knowledge and adequate human resources to operate the mines competently.

In 2010,Tanzania’s parliament passed a new mining law requiring the government to hold an equity stake in all new mining projects. As a result, when its mining license came up for renewal in 2012, TanzaniteOne was forced to give up 50% of its equity. Executives at the firm believe there may be a silver lining to this, as the government now has an incentive to actively enforce the laws meant to protect the industry. For example, the government could decide to curtail illegal smuggling, which is a huge issue that adversely affects the entire industry.

TanzaniteOne would be in a unique position to benefit from such a policy change because of its investment in a polishing facility. One of the expert gem cutters at the facility noted that, as the largest miner of tanzanite, TanzaniteOne has the scale needed to make such a venture profitable. The company has also been quite astute in its willingness to buy stones from other miners for cutting and polishing. TanzaniteOne is a pioneer in its decision to move up the production and distribution chain, where greater added value resides. While the cutting-and-polishing side of the business is not included in the stake ceded to the government, TanzaniteOne will, by virtue of its partnership with the state, have more leverage when asking for stricter enforcement of the export ban.

A Detriment to the Market: Tanzanite Pricing and Rarity

The mining area where tanzanite is found is divided into four sections, or blocks, labeled A, B, C, and D. TananiteOne has the concession for Block C, the largest of the four. The other blocks are occupied and exploited by an assortment of medium and small, independent, and artisanal miners. With little in the way of capital investments or even general overhead, these miners are able to flood the market with cheap gemstones and depress the overall price of tanzanite stone. Hayley Henning, executive director of the Tanzanite Foundation, agrees that the availability of stones of dubious provenance at huge discounts is detrimental to the entire market. Once its stones reach the market, TanzaniteOne has no way to differentiate its products from those of the other miners, putting it at a disadvantage in price negotiations.

Moreover, tanzanite’s rarity has ironically worked against it as the stone is still relatively unknown. The Tanzanite Foundation, a nonprofit founded by TanzaniteOne, has worked tirelessly to increase awareness, issuing certificates of authenticity that guarantee a stone’s origin and characteristics. Like diamonds, tanzanite stones are also rated for their clarity, color, carat, and cut. Unlike diamonds, they can be certified to be conflict-free. In addition, the TanzaniteOne mine adheres strictly to labor laws and uses technology to minimize its environmental impact.

Through the Tanzanite Foundation, TanzaniteOne has also been involved in numerous social projects that benefit the surrounding community. Among the most noteworthy, the mine has provided fresh water to the neighboring areas. In addition, it has given financial support to local schools, a medical clinic, and a community center. Henning describes another project that empowers local Maasai women by helping them make artisanal jewelry that is then sold internationally. And yet these projects do not promote TanzaniteOne’s stones directly. As with pricing, it is impossible to tell TanzaniteOne stones apart from those mined by others. Thus, many of the Foundation’s efforts benefit the entire industry.

TanzaniteOne has attempted to emulate business models developed in the diamond industry by selling its stones through sightholders, the companies authorized as bulk purchasers of rough diamonds. According to a sales manager for TanzaniteOne, the company — as the largest miner of tanzanite — believed it could shape the market for the stone and influence its market price by partnering closely with a limited number of carefully selected international gemstone wholesalers. Its size notwithstanding, TanzaniteOne lacks the volume to set a price for tanzanite. In fact, the sightholders yield far more power in the relationship, as they can easily obtain stones from the other miners.

TanzaniteOne has attempted to emulate business models developed in the diamond industry by selling its stones through sightholders, the companies authorized as bulk purchasers of rough diamonds.

In 2012, TanzaniteOne’s situation became dire. As detailed in its parent company’s annual report, illegal miners from the other blocks infiltrated Block C and focused on the higher-quality areas of TanzaniteOne’s mining operations. The invasions were aggressive and violent, and included the use of firearms and explosive devices. Several employees were injured, and a security guard was maimed. TanzaniteOne received little support from the authorities and found it difficult to enforce its property rights.

Without the full backing of the state, any enforcement action had the potential to blow up into a public relations disaster. TanzaniteOne was also aware of the high level of violence a response could trigger and was concerned for the safety of its employees. It decided to retreat from those mining areas at great financial cost. When its mining license came up for renegotiation in 2012, the company made a bold but costly decision. Instead of entering a protracted and contentious dispute, it agreed to cede 50% of the license to the Tanzanian government, in accordance with the new mining act. Henning noted that, as a part owner, the government would now have a powerful incentive to step in and help enforce TanzaniteOne’s property rights. But it still meant that Richland Resources took a significant write-off to reflect the new arrangement. As a result, trading of its stock was suspended temporarily.

On July 18, 2013, the Tanzanian police began an operation to evict the illegal miners from the areas that belonged to TanzaniteOne. It seemed that the company’s gamble was paying off. By the next day it was able to reclaim an area from which it had previously retreated. On July 21, however, a TanzaniteOne employee was fatally shot by illegal miners in the presence of the police — an example of how complex and difficult the situation is for the company.

TanzaniteOne is, first and foremost, a mine operator. But it has realized that there are far better rewards for those positioned higher up the value chain. Just as it saw an opportunity to move into gem polishing and cutting when the export ban was enacted, it also realized the advantages of becoming a retailer and launched stores under the brand Tanzanite Experience. This new channel of business has helped to counteract the negative effects facing the mining operations. Currently, about 80% of the company’s revenues comes from selling rough stones, but retailing yields better profitability.

As they look to the future, all parties involved acknowledge the need to leverage the current supply of tanzanite to build a sustainable and resilient industry.

Retailing has also allowed TanzaniteOne to forge partnerships with designers of fine jewelry. This market is far more stable than mining and has better long-term prospects. As they look to the future, all parties involved acknowledge the need to leverage the current supply of tanzanite to build a sustainable and resilient industry. This can be achieved by moving into strategic sectors such as cutting, polishing, and retailing, where the profit margins are higher.

The sales channels for tanzanite are currently controlled mostly by the sightholders, who can leverage their buying power through their access to numerous miners. In a sense, the sightholder business model fuels the underground trade in rough stones. As TanzaniteOne continues to develop its footprint in retailing, it will achieve greater market power.

Finally, the tanzanite industry has the potential for enormous growth due to untapped international markets, particularly in China and India. According to a recent study by Bain & Company, both of those jewelry markets are growing at a rapid pace. In contrast to the U.S. and Europe, where diamonds are more popular, consumers in these regions prefer colored gemstones and buy them at a rate four times greater than diamonds. The trichroic property and rarity of tanzanite also gives the gem a competitive edge in these markets. In India it is a substitute for sapphires, which astrologers believe to have negative properties. Because the retail jewelry network in emerging markets is not as well-established as in developed markets, it makes more sense to utilize the strength of current relationships with sightholders to optimize interest in tanzanite.

An Opportunity to Turn the Industry Around

Tanzanite appears to have all the elements of a hit product — supply rarity, unique trichroic properties, and a foundation dedicated to social impact. Yet, nearly 50 years after its discovery, a market breakthrough continues to elude the stone. The reason lies in the Tanzanian government’s role, as illustrated by the history of the industry and the case of TanzaniteOne, the owner of the largest tanzanite deposit in the world. The company serves as a powerful example of the importance of good governance, and how the lack of enforcement can potentially destroy an industry by leading to erratic pricing, disruptive competition, and an unbalanced distribution of power among the players.

Although TanzaniteOne managed to maintain its leading position in the industry despite challenges of the past, it now faces an additional hurdle in the form of a new partnership that has cost the company half its equity. However, with the right development, this new collaboration can become the opportunity to turn the industry around. Now that the government has a 50% stake in the company’s livelihood, TanzaniteOne has the leverage to demand enforcement against illegal trading. That alone is not enough, as the company also needs to increase its retail presence in existing U.S. and European markets to rebalance its relationship with sightholders. In contrast, in emerging markets such as China and India, collaboration with sightholders is key for growing the market and increasing demand.

The future of both tanzanite and the livelihoods of those who work within the industry or live in the areas surrounding the mine depends on TanzaniteOne’s success and its ability to change the mindset of its partners while bringing forth the true value of the gemstone.

This article was written by Diego Rimoch and Stephenson Cherng, members of the Lauder Class of 2015.