In this opinion piece, Wharton finance professor Michael R. Roberts argues that a basic understanding of finance will help students and their parents avoid making disastrous decisions, such as taking on excessive student loans.

The student loan crisis has been in the news for some time now. A recent Wall Street Journal article describes the financial disaster befalling graduate students strapped with debt that they will never be able to repay and the taxpayers who will end up paying for those unpaid loans. However, this is just one example of the many life-altering financial decisions young (and old) people make and the implications of those decisions that extend beyond the decision-makers. That many people make financial decisions with little understanding of their implications is why finance should be mandatory for every high school student.

Now, as a finance professor, I realize that statement sounds terribly self-serving, but it shouldn’t be controversial, and I speak from experience. I took out student loans to support my graduate education with no clue of the future financial burden. I got lucky. My loans were modest in size, and I got a job that allowed me to pay down my loans quickly. What I should have done before taking out the loans was spend an hour or two figuring out my future loan payments and whether I would be able to afford them with my job prospects after graduation.

Let’s perform this exercise to illustrate how easy and informative it can be using the Columbia graduate film program highlighted in the Wall Street Journal article as an example.

How much do we have to borrow to complete the program? That depends on the cost of the program and living expenses less any money we contribute. While estimating how much we will owe when we graduate would appear straightforward, there are a couple of wrinkles. First, loan fees are often deducted from what we borrow. In other words, we must borrow more than what we need to cover these fees. Second, interest accrues on the loans as soon as you receive the money, a feature common to most loans. The result is that students are often surprised (shocked) to see that their outstanding balance after graduating is significantly larger than what they thought the cost of their education would be.

“That many people make financial decisions with little understanding of their implications is why finance should be mandatory for every high school student.”

The Columbia program currently costs approximately $70,000 plus another $30,000 in living expenses. Let’s assume that these costs don’t change next year, and we don’t have any money to defray these costs. Let’s also assume that there are no borrowing fees, and we need to borrow all our expenses for each year at the beginning of the year. In other words, we borrow $100,000 at the start of the program, and another $100,000 one year later.

Current federal loan rates are around 6%, according to the Federal Student Aid website. When we graduate in two years, we will owe the federal government approximately $100,000 x 1.062 + $100,000 x 1.06 = $218,360. The accrued interest results in over $18,000 of additional money we owe upon graduation, assuming we have not been making payments while in school. Consider longer programs, like law and medical, and you can understand the sticker shock at graduation.

Now, let’s figure out what our monthly payments will be when we graduate. There are lots of payment plans and variations on how interest compounds, but ultimately the size of our loan payments will be primarily a function of how quickly we can pay off the loan.

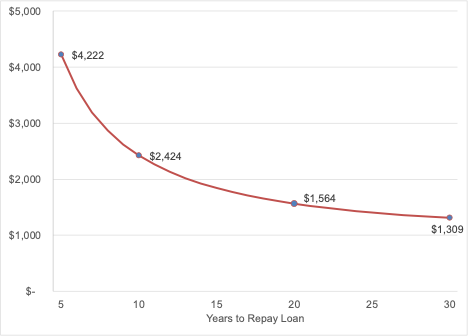

Figure 1: Monthly Loan Payments for Different Repayment Horizons

Figure 1 shows how monthly payments vary with the time to repay the loan; longer payment plans, lower payments.

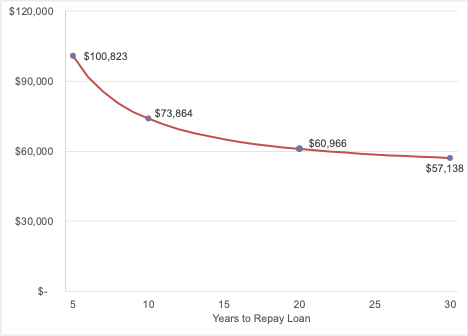

Armed with this knowledge we can estimate how much we must earn to pay off our loan and afford living expenses after graduation. Assuming a 10-year payment plan, we are looking at a little under $30,000 per year in loan payments. If our annual living expenses are similar in size, then we will need about $60,000 per year after taxes to cover our loan payments and living expenses. At an effective tax rate of 20%, these needs require an annual gross salary of $75,000. Figure 2 shows the gross income requirements as we vary the time to repay our loan and therefore the size of the monthly payment.

Figure 2: Gross Income Required to Afford Loan Payments and Living Expenses

Now it’s time for a reality check: Is our degree going to lead to a job with a gross income necessary to repay the loan and provide a living income? While we can’t know for certain, we can understand the risk we are taking. Most schools will, or should, provide information on job placement and average salaries for their different programs. So, we can determine how likely we are to get a job that covers our future expenses.

Of course, there’s still uncertainty even with a thoughtful bit of financial analysis. Perhaps we’ll graduate in a recession and have difficulty finding a job or face lower wages. Perhaps personal circumstances will change in a manner affecting our job prospects. These uncertainties don’t negate the importance of careful financial thought before a big decision, they amplify it!

“While we can’t eliminate uncertainty, we can prepare for it.”

The analysis above shows that we can take a lower paying job by simply stretching the payments over a longer horizon. It also shows us the minimum amount we must earn to cover our loan payments and living expenses. By changing some of the numbers and assumptions, we can ask a myriad of “what if” questions. What if we take a teaching position during our studies to reduce some of the costs? What if we use some of our savings to reduce our loan size? More generally, finance provides a simple framework within which we can make important decisions from a position of clarity and understanding. So, while we can’t eliminate uncertainty, we can prepare for it.

The focus here on student loans, while illustrative, is not unique. Auto loans and leases, home loans, credit cards, saving and investing, planning for retirement, etc., are all examples in which a little financial thought early on can pay huge dividends – pun intended – later. Importantly, the analysis done here, while approximate, is not only informative but easy to perform. The calculations require nothing more than arithmetic and could be performed by most children in middle school.

Imagine a generation of teenagers and young adults prepared to engage with financial realities.