It’s not even summer driving season yet and gas prices are already climbing. Prices at the pump have increased 52 cents this year, and now stand at an average of $3.81 a gallon, surpassing $4 a gallon in several states and pushing uncomfortably close to the all-time high of $4.11 set in July 2008. Pundits are predicting gas could hit $5 a gallon before the end of the year. Frustration is rising along with the cost of oil as Americans look for someone to blame.

Fingers are pointing in all directions: from Iran to China, Washington to Wall Street. In a recent national survey by the Pew Research Center and The Washington Post, when asked who is most responsible for rising gasoline prices, 18% of Americans pointed to President Obama and his administration, 14% fingered oil companies, 11% chalked it up to tensions with Iran or the threat of war or upheaval in the Middle East, and 4% pegged it on speculators or excessive Wall Street trading.

There is no single cause for oil to rise, say Wharton professors and energy experts. Overall, fluctuations in oil prices boil down to supply and demand. The world is “pushing up against what’s available in terms of producible oil,” says Robert Ready, a finance professor at the University of Rochester’s Simon School of Business who studies oil supply shocks. As oil becomes more expensive to tap and the world demands more of it, there is increasing strain on the available supply, Ready notes. That means a single unexpected event — whether unrest in the Middle East, a pipeline explosion or a hurricane in the Gulf — can disrupt supply and send prices higher. “There just isn’t slack out there,” he says.

About a year ago, upheaval in Libya triggered a run-up in oil prices. This year, all eyes are on Iran, which is under pressure from the United States, Israel and Europe to suspend its nuclear research program. In February, a defiant Iran threatened to block the Strait of Hormuz, a narrow passage to the Persian Gulf that yields access to 20% of the world’s oil.

“Everybody is concerned that the Middle East could blow up in an unanticipated way,” notes Howard Pack, a business and public policy professor at Wharton and co-author of The Arab Economies in a Changing World. The Middle East produces about 30% of the world’s oil, so instability in the region can impact supply and drive up prices worldwide. Iran’s nuclear program is only one potential problem; some accuse Iran of stoking Shiite opposition to the government in Bahrain and fomenting Shiite unrest in East Saudi Arabia. “It’s pretty clear that all the Sunni Arab countries are very worried about Iran,” says Pack. “I think everybody is quite convinced that Iran is trying to develop a nuclear weapon.”

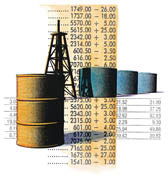

Seasonal Gas Prices: Summer vs. Winter

Nevertheless, Iran is not the “dominant explanation” for rising oil prices, according to Pack. “More fundamentally, we still have this very rapid growth in China … and India continues to grow,” he points out. According to Bloomberg News, China is building four emergency petroleum reserves and planning to stockpile more oil to help reduce price fluctuations locally. Such growing economies will push demand higher and “will undoubtedly have an impact on oil prices,” Pack says.

And that, of course, means higher gas prices for consumers. It takes about two weeks for crude prices to trickle through the distribution stream, notes Avery Ash, manager of regulatory affairs for AAA, the Heathrow, Fla., nonprofit that provides travel and roadside assistance. For every $1 a barrel increase in the price of crude, consumers can expect to see an increase of about two and a half cents for each gallon of gasoline.

The price at the pump does not always correspond directly to a barrel of oil. Some price increases for gasoline are seasonal, Ash points out. In the U.S., for example, gas prices increase in the summer because gasoline is blended differently to reduce air pollution. The Environmental Protection Agency requires all gasoline sold after June 1 to be a “summer grade” gasoline, a blend that contains more additives and less butane than winter-grade gasoline. Because of its different ingredients, winter gasoline blends are about 6 cents a gallon cheaper to produce than summer blends, Ash says.

Last summer,a rapid increase in crude production in North Dakota and Canada created a backlog at the nation’s oil storage facilities in Cushing, Okla., which funnel much of the nation’s crude to refineries on the Gulf Coast. A shortage of pipelines linking Cushing to Gulf Coast refineries caused the backup, Reuters reported at the time. For a while, the local oil glut pushed the price of West Texas Intermediate (WTI) crude oil, the U.S. crude benchmark, to record levels below Brent Crude, the benchmark for gas prices in Europe, the Middle East and much of Africa. Brent relies on oil from the North Sea and is refined primarily in northwest Europe. The spread between the two benchmarks widened to almost $30 per barrel.

While the two benchmarks are much closer today, regional disparities in gas prices persist from state to state. Refineries that supply Western states such as Colorado and Wyoming have access to cheaper crude oil than refineries in the Northeast, for example. “So they can make significantly cheaper gasoline,” Ash notes. “That’s the reason you’re seeing crude products in the center of the country selling for significant discounts.”

Denver currently has the lowest average gas price in the country, at $3.36, according to Lundberg Survey, a Camarillo, Calif.-based company that tracks fuel prices by surveying gas stations nationwide. The highest was Los Angeles at $4.35. Gas prices in California are more expensive than in other parts of the country due to higher taxes and stringent environmental regulations.

Getting more oil online won’t happen quickly. New supplies have been discovered in the tar sands in Canada, shale oil in the U.S. and pre-salt deposits in Brazil, but extracting it could take time. “We have all sorts of new supplies we’ve discovered, but they’re years away from being in the market,” says Wharton management professor Witold Henisz. “The stuff we’re finding now is much more expensive [to extract], and we’re not finding lots [of it]…. You’re exploring in more difficult places…. In the short term we still face supply constraints.”

If the price of gas goes up too high, it could impact the economic recovery, says Henisz. Compared with a lot of other goods, “the demand for gas is relatively inelastic,” he notes. People still have to fill up their cars to get to work or pick the kids up from school. But once the price passes a “symbolic threshold,” it will dampen demand because consumers will start cutting back. “No one’s turning the heat off, but they are changing the temperature.” People may start carpooling, he adds, and restaurants “will get hit. All of these decisions add up.”

The “threshold” for such belt tightening used to be $2 or $3 per gallon. Today, the magic number may be $5. On average, Americans say that gas prices of $5.30 to $5.35 per gallon would make them cut back on spending, according to a Gallup Poll conducted in early March. In the same poll, 85% said the President or Congress should “take immediate actions to try to control the rising price of gas,” although only 65% said they believe that government officials could actually do anything to keep prices from going up.

Politics, As Usual

As the November election approaches, the discussion has grown increasingly political. Republicans say gas prices are soaring because the Obama administration has crippled the energy industry by blocking or hindering exploration and new energy projects,such as TransCanada Corporation’s Keystone XL pipeline. The White House counters that domestic crude oil production is at its highest level in eight years, and oil imports have declined since Obama took office. Obama has called for a repeal of $4 billion in annual government subsidies to the oil industry and says he is working to prevent speculators from distorting prices.

On March 5, 23 senators and 47 House members sent a letter to the Commodity Futures Trading Commission, saying that regulators needed to do more to stop Wall Street futures traders from dominating the oil market. “[E]xcessive oil speculation significantly increases oil and gasoline prices,” the letter reads. “[O]il speculators now control over 80% of the energy futures market, a figure that has more than doubled over the past decade.”

Joseph R. Mason, chair of banking at the E.J. Ourso College of Business at Louisiana State University and a senior fellow at Wharton through the Wharton Financial Institutions Center, says a change in regulations might help. “Without a doubt, the Fed’s monetary policy continues to cause uncertainty, spurring investors to look for ways to park their assets in oil futures,” Mason wrote in a recent article in U.S. News & World Report titled, “What Obama and Ben Bernanke Should Do about Gas Prices.”

Low interest rates make it difficult for investors to generate earnings, so they are looking for higher-yield investments in commodities such as oil, Mason notes. “There are investment opportunities in the oil sector that are very valuable,” he says, which means that people are putting money there rather than building factories and creating jobs. Raising interest rates could also help reduce the volatility in gas prices in the U.S. by incentivizing more domestic production that would reduce pressures at the pump, Mason argues. “Increasing oilprice stability may still allow increases in the price of oil … but makes it less subject to price shock and volatility,” he told Knowledge at Wharton in an interview. “It can’t completely mitigate the price shock, but it could help.”

Where do oil prices go from here? That depends on what happens next in the Persian Gulf, according to Bernard Baumohl, chief global economist at the Princeton, N.J.-based Economic Outlook Group and author of The Secrets of Economic Indicators: Hidden Clues to Future Economic Trends and Investment Opportunities. “If there is going to be a military confrontation [with Iran], we are looking at world [WTI] prices moving up to $130 per barrel,” he says. (On Wednesday, WTI Spot was $106.07 a barrel.) A longer, more extensive conflict could send prices to $150 or even $200. It’s impossible to predict with certainty. “There’s so much we don’t know,” he says.

President Obama may choose to tap the Strategic Petroleum Reserve if the average price of gasoline climbs above $4 a gallon, Baumohl suggests. In August and January 2011, Obama authorized the sale of 30.64 million barrels from the reserve in response to supply disruptions due to unrest in Libya. With a capacity of 727 million barrels and currently holding 695.9 million, the Strategic Oil Reserve is the largest stockpile of government-owned crude oil in the world.

Rising fuel costs are “definitely going to put a dent in consumer spending” if they continue, Baumohl says. “For every penny increase at the pump, Americans spend an extra $4 million a day” for gasoline, he notes. That adds up to about $1.5 billion per year. Within one to three months, an increase in oil prices is reflected in the economy, in everything from higher transportation costs to price increases for petroleum-based products such as plastic combs.

“Less than 5% of take-home pay actually goes to paying for gasoline,” Baumohl points out, “But gasoline prices have a much greater psychological impact on consumers because they see on a daily basis how much the price of gasoline goes up. It’s advertised on so many signs.” The uptick in prices thus has a “palpable impact” on consumers, he says.

In many ways, the run up of gas prices this year is similar to last, when the Arab Spring raised fears of an unstable Middle East. “The only difference is that there is one huge conflict out there that is a much greater danger than last year, that is, [the possibility of] an actual war taking place in the Persian Gulf,” Baumohl says. “We could actually see a clash, and because we’re that much closer to a confrontation, it makes 2012 a bit more ominous than 2011.”